As we look toward 2026, we first reflect on a year defined by exceptional volatility and a complex geopolitical landscape. Throughout 2025, prolonged conflicts in the Middle East and Ukraine kept global risk premia elevated, while persistent inflation across developed markets constrained monetary policy flexibility.

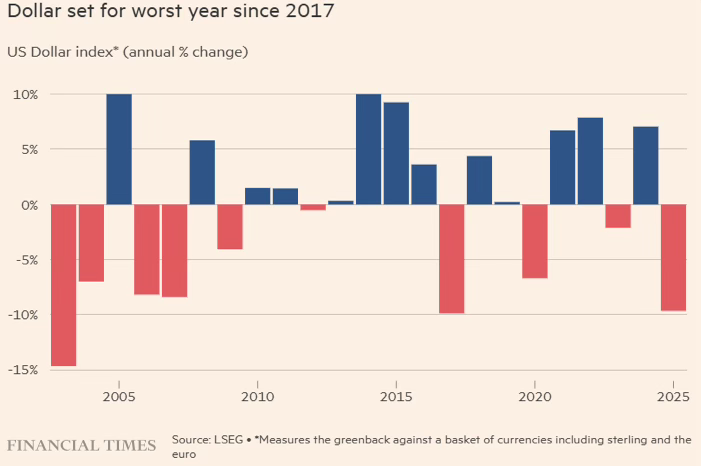

The primary source of market turbulence, however, was the unpredictability of U.S. policymaking. This uncertainty peaked on April 2nd, when the administration initiated a sweeping and punitive global tariff campaign, targeting allies and rivals alike. Concurrent public pressure on the Federal Reserve further challenged central-bank independence, creating a climate of instability that led to one of the weakest years for the US dollar in the modern floating-rate era.

Despite this turbulent backdrop and the resulting fluctuations in equity across our portfolio, our strategies remained highly resilient. We are proud to report that nearly all our systems outperformed their respective benchmarks—often by significant margins. Most notably, our models maintained high efficiency on a risk-adjusted basis, successfully navigating the year’s most volatile periods to deliver strong results for our clients.

The greenback is currently on pace for a roughly 9.5% annual decline against a basket of major currencies—its most significant retreat since 2017. This downturn reflects a fundamental shift in market sentiment, as escalating trade-war anxieties have not only dampened the U.S. growth outlook but also compromised the dollar’s long-standing status as a reliable safe-haven asset.

The Euro emerged as the primary beneficiary of this shift, surging nearly 14% to surpass $1.17—its highest level since 2021—while Sterling and other major currencies recorded substantial gains. The greenback’s descent began in earnest following the April tariff shock, at one point collapsing nearly 15% before finding a temporary floor. However, a renewed structural downtrend took hold in September as the Federal Reserve resumed rate cuts. This environment fueled a massive rally in EUR/USD, GBP/USD, and gold, with the latter hitting a historic peak above $4,549 in December. By year-end, foreign exchange markets had fundamentally repriced: global capital flows are now driven less by interest-rate differentials and more by the perceived credibility of U.S. policy.

Looking into 2026, the dollar’s trajectory hinges on the upcoming appointment of the next Federal Reserve chair. If the succession is viewed as a compromise of central bank independence or a pivot toward political pressure for deeper cuts, the structural headwinds of 2025 may persist. Such a scenario would likely result in continued volatility and tactical repricing across all major pairs rather than a return to predictable, directional trends.

Nevertheless, as markets distance themselves from peak policy uncertainty and rate expectations stabilize, we anticipate a gradual return to macroeconomic equilibrium. More transparent policy signaling and normalized liquidity should foster a more orderly trading environment. Historically, these transitions favor adaptive, risk-controlled systematic strategies that can navigate both trending and range-bound markets. With our refined framework and disciplined execution, we believe the landscape for 2026 is increasingly constructive for delivering consistent performance.

December Review: Policy Speculation and Year-End Volatility

After a two-month lull in economic data, December featured a dense slate of releases that catalyzed the U.S. dollar’s sharpest annual decline since 2017. Rather than reacting to isolated data surprises, markets focused on the long-term viability of monetary policy paths heading into 2026. As disinflation gained momentum and global growth signals diverged, price action was increasingly dictated by a fundamental reassessment of central-bank credibility and forward guidance. Within this landscape, the U.S. dollar remained the primary focus, with major currency pairs and gold moving in lockstep with evolving expectations for U.S. interest rates.

The dollar began the month under immediate pressure. Between December 2nd and 3rd, the U.S. Dollar Index (DXY) drifted lower as investors questioned the sustainability of U.S. rate support. This shift was fueled less by economic prints and more by mounting concerns over the future of the Federal Reserve. Speculation intensified that White House adviser Kevin Hassett might succeed Jerome Powell as Fed Chair in 2026—a prospect markets interpreted as a potential threat to central-bank independence and a signal of structurally lower rates ahead.

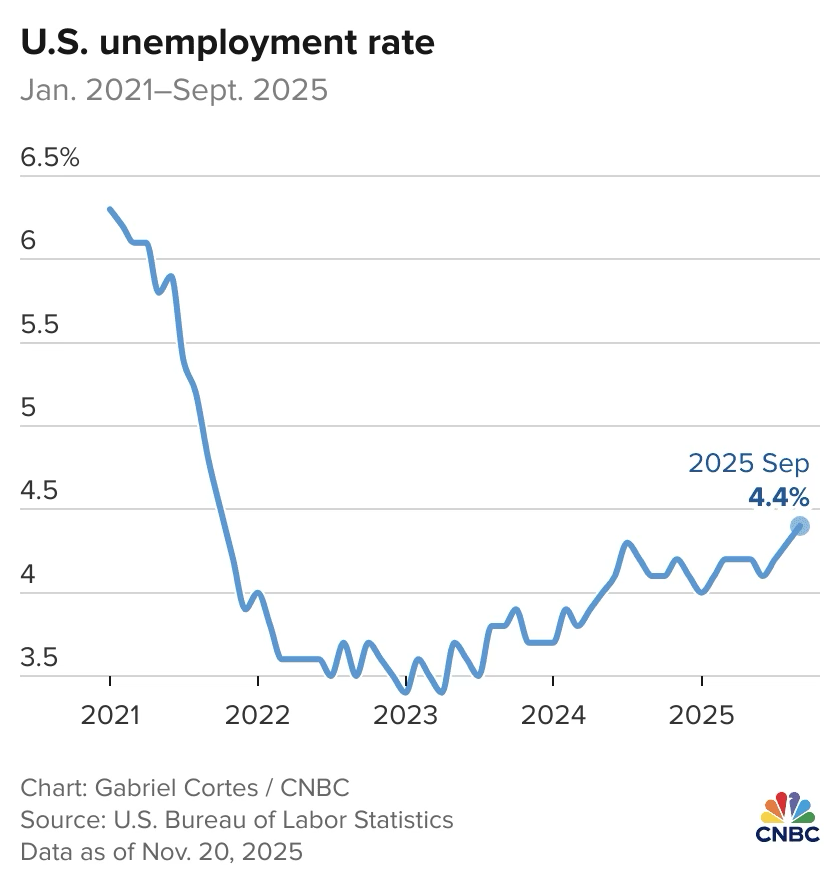

These policy concerns were further compounded by softening labor market signals. With November ADP employment figures expected to fall to just 5k (from a previous 42k) and the ISM Services PMI projected to ease to 52.1, the greenback entered the final weeks of the year in a vulnerable position. This combination of political uncertainty and a cooling economy solidified the narrative of a dollar in transition, setting the stage for the tactical opportunities that defined the close of 2025.

Between December 3rd and 9th, the US dollar traded within a narrow range as market participants moved to the sidelines ahead of the December 10th FOMC meeting. Despite this lack of directional conviction, a bearish undertone persisted as expectations for a rate cut continued to solidify.

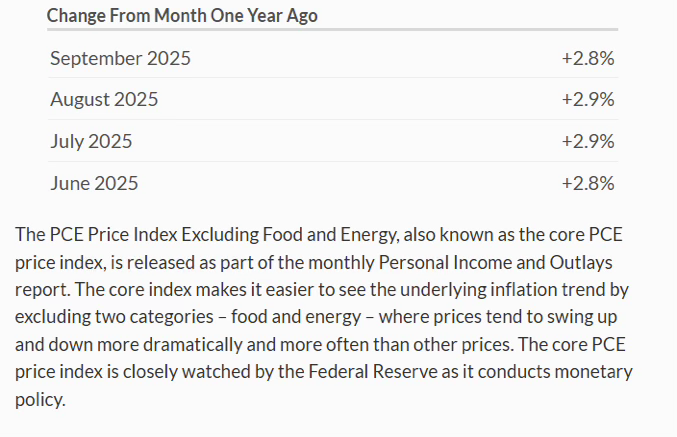

Investor sentiment was heavily influenced by delayed September data, which revealed that core PCE inflation had cooled to 2.8% year-over-year. This reading—the Fed’s preferred inflation metric—aligned with the broader disinflation narrative and reinforced the view that price pressures were successfully converging toward target. By December 8th, CME FedWatch pricing reflected a nearly 90% probability of a 25-basis-point cut. This high level of certainty effectively capped any potential dollar recovery, even as U.S. consumer sentiment showed a modest, albeit marginal, improvement toward the end of the week.

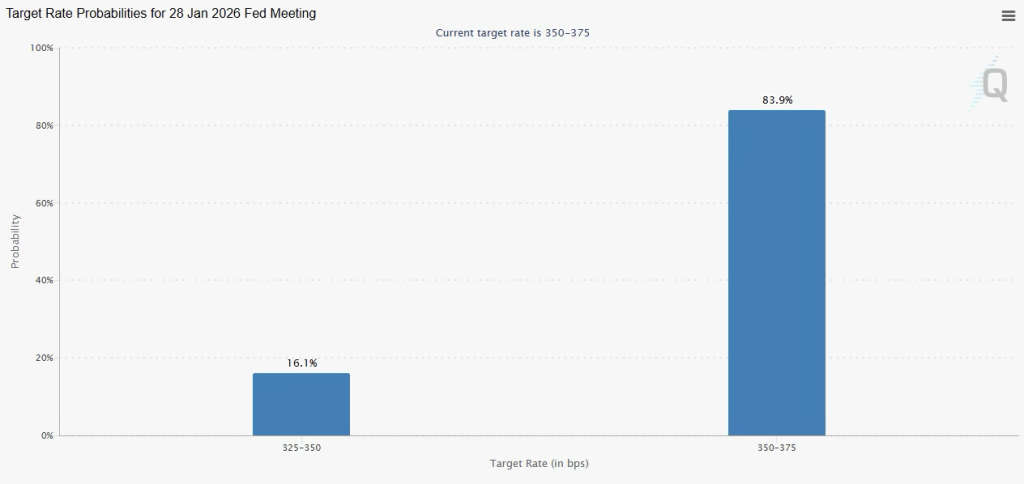

The month’s defining inflection point occurred over December 10–11, when the U.S. dollar sold off sharply following the Federal Reserve’s decision to cut interest rates by 25 basis points. This move brought the target range to 3.50%–3.75%, marking the third consecutive reduction of late 2025. While the cut was widely anticipated, the market’s focus shifted to the growing internal friction within the FOMC, which saw an unusual 9-3 vote split—the highest level of dissent in years.

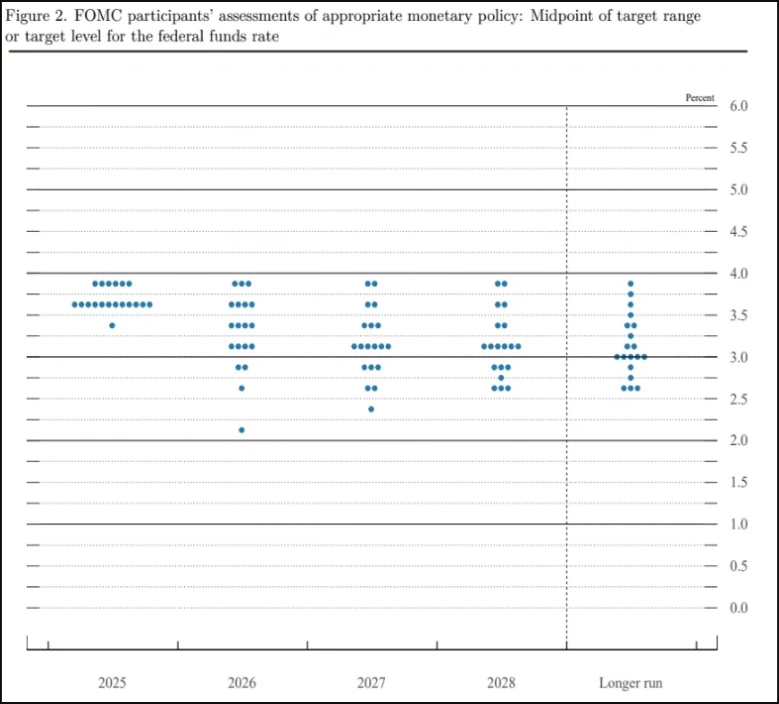

Chair Powell’s subsequent press conference offered less support for the dollar than hawks had hoped. Although the Fed’s updated “dot plot” signaled only one additional cut for 2026, Powell adopted a distinct “wait-and-see” posture, citing the need to gauge the long-term impact of recent policy easing. This conservative forward guidance created a notable disconnect with market participants, who continued to price in a more aggressive easing cycle.

Furthermore, Powell’s admission that job growth may have been overstated since April injected fresh doubt into the dollar’s outlook. By signaling that the Fed was now within the “range of neutral,” the meeting effectively confirmed that the era of restrictive U.S. rates was ending. This shifted the dominant market narrative from interest-rate differentials toward concerns over U.S. economic growth and policy independence, leaving the greenback fundamentally weakened as it moved toward the year-end.

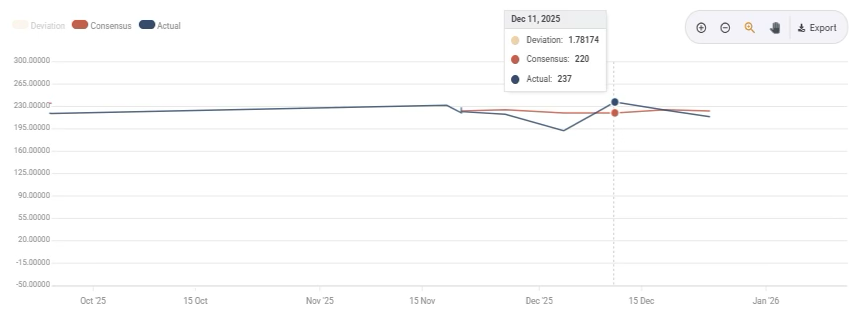

This divergence intensified dollar selling, particularly after weekly initial jobless claims jumped to 237k—significantly exceeding the 220k forecast. The spike reinforced the market’s perception that labor-market slack was emerging more rapidly than Fed officials had projected, further undermining the greenback.

From December 11–21, the dollar consolidated at lower levels as a series of heavy data releases failed to restore market confidence. While November non-farm payrolls modestly beat expectations at +64k (versus 50k forecast), this was overshadowed by the unemployment rate ticking up to 4.6% and a noticeable loss of consumer momentum. Retail sales further disappointed, printing flat at 0.0% against a projected 0.1% increase, signaling softer domestic demand. Although the payroll beat provided a brief moment of stability, the overarching narrative of cooling labor conditions and stagnant consumption kept the DXY capped, resulting in range-bound trading near its recent lows.

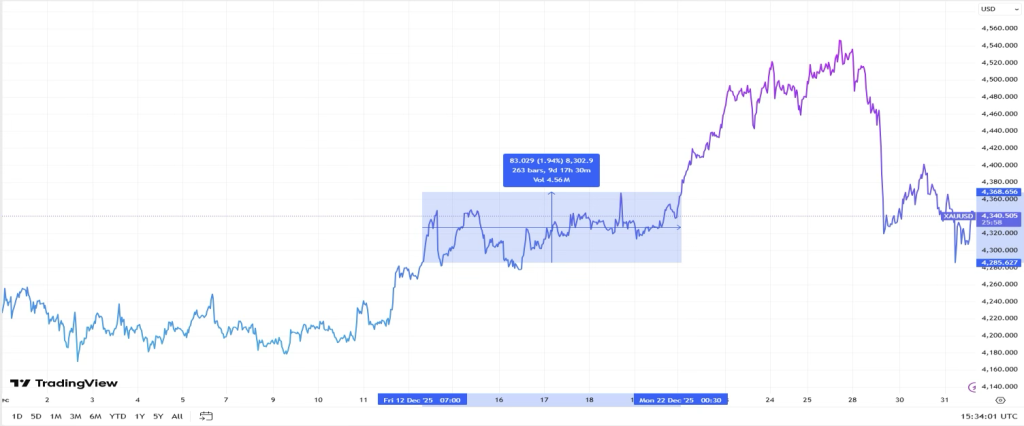

This consolidation broke between December 22nd and 24th as the dollar resumed its decline. Markets largely ignored the stronger annualized Q3 GDP growth of 4.3%, focusing instead on the 2026 easing cycle. Expectations for further Fed cuts gained traction, while geopolitical tensions directed safe-haven flows toward precious metals rather than the greenback. Selling pressure intensified after Trump reiterated that any future Fed Chair must commit to significant rate cuts even in a robust economy, heightening concerns over long-term policy independence. As markets priced in at least two additional cuts for 2026, the DXY slid to its lowest level since early October.

From December 24th through year-end, the dollar settled into a tight range as holiday liquidity thinned and attention shifted toward the 2026 outlook. The DXY hovered near the 98.0 level, caught between persistent easing expectations and intermittent geopolitical headlines, ultimately closing the month on a significantly weaker footing. These evolving expectations around U.S. rates and policy direction acted as the primary catalyst for moves across major currency pairs and gold.

EURUSD

EUR/USD opened December with a firm tone as the dollar softened, driven by rising confidence that U.S. macroeconomic momentum was cooling and that a December policy pivot from the Federal Reserve was effectively a certainty. Meanwhile, Euro-area data remained broadly stable, reinforcing the view that the ECB could remain comfortably on hold. This allowed the Euro to capitalize primarily on dollar weakness rather than domestic strength.

Between December 4th and 10th, the rally stalled as EUR/USD drifted sideways with a mild downward bias, reflecting growing caution ahead of the Fed meeting. The prevailing dollar sell-off paused while investors reduced exposure and sought confirmation rather than continuing to trade on anticipation. Mixed U.S. releases, combined with softer activity signals from the Euro-area, reinforced this holding pattern and kept the pair range-bound and slightly defensive.

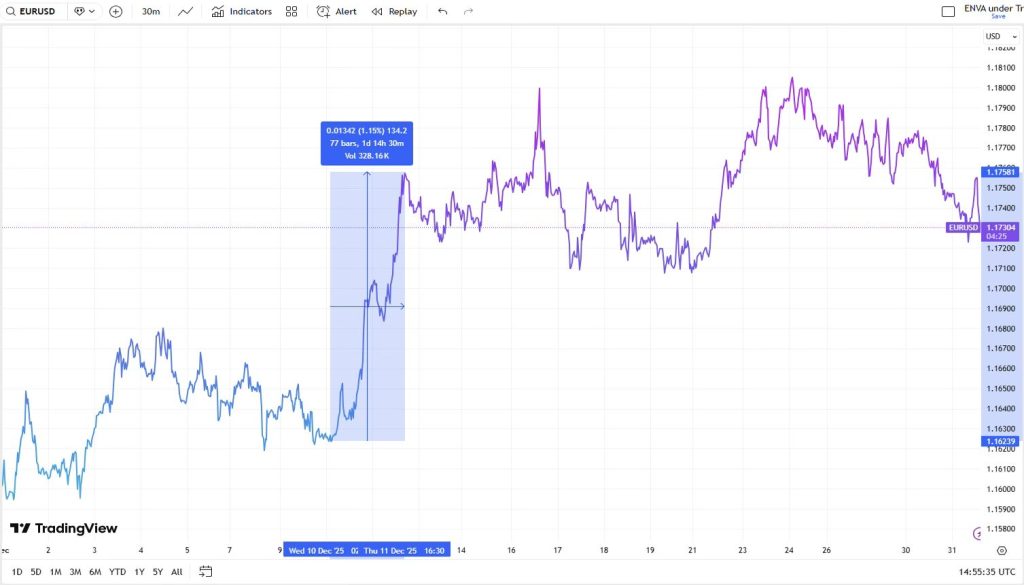

This hesitation gave way on December 10–11, when EUR/USD rallied sharply following the Federal Reserve’s third consecutive 25bp rate cut, which lowered the target range to 3.50%–3.75%. The move gained further momentum after weekly jobless claims rose to 236k (exceeding the 220k forecast). This data strengthened the perception of emerging labor-market slack in the U.S., accelerating the broad-based repricing of the dollar to the downside.

The rally proved short-lived, however, as the pair slipped into choppy consolidation between December 11th and 22nd, albeit at higher levels. Aside from a better-than-expected non-farm payrolls print, subsequent data—including higher unemployment and weaker retail sales—pointed to a softening U.S. labor backdrop. Headline CPI slowed to 2.7% year-over-year, undershooting expectations but largely confirming the disinflationary trend that had already been priced into the market.

At the same time, the ECB kept policy unchanged, while softer Euro-area PMIs on December 16th signaled moderating growth. These factors capped the Euro’s upside, resulting in uneven, two-way trade.

A brief rally emerged between December 22nd and 24th, driven primarily by renewed U.S. dollar weakness rather than Euro-specific catalysts. The greenback softened as markets leaned into the expectation that the Fed would continue its easing cycle well into 2026—a trend reinforced by surging demand for precious metals as gold reached record highs above $4,549 amid elevated geopolitical tensions. This backdrop overshadowed otherwise upbeat U.S. growth data, including a third-quarter GDP print of 4.3% annualized, as investors prioritized the long-term policy trajectory. Furthermore, comments from Donald Trump advocating for rate cuts even in a strong economy amplified concerns regarding the Fed’s future independence, further undermining the dollar and allowing EUR/USD to press higher into the holiday break.

From December 24th through month-end, EUR/USD returned to sideways trading with a slight downward tilt as volumes dropped sharply and macroeconomic catalysts subsided.

GBPUSD

GBPUSD also started December on a firmer note as the US dollar softened on growing conviction that the Federal Reserve was approaching an easing pivot. Early gains came despite a mixed UK backdrop, with UK composite PMI easing to 51.2 in November from 52.2, signaling slower but still expansionary momentum. With no immediate negative surprises at home, sterling was able to ride early-month USD weakness.

That momentum faded between December 4th and 10th, as GBP/USD entered a cautious, sideways phase ahead of the Federal Reserve meeting. Domestic data acted as a modest headwind; the ONS reported that GDP contracted by 0.1% in October, with output also declining 0.1% over the three-month period. These figures reinforced the UK’s fragile growth profile and kept the pair on the defensive as the market’s initial optimism cooled.

The tone shifted sharply on December 10–11 after the Federal Reserve delivered a 25bp rate cut, lowering the target range to 3.50%–3.75%. Downward pressure on the dollar intensified as weekly initial jobless claims rose to 236k—surpassing the 220k forecast—which strengthened the case that U.S. labor conditions were cooling. This data accelerated the repricing of U.S. rate support, allowing GBP/USD to break higher. The move was primarily a reflection of broad-based dollar weakness rather than a shift in underlying UK fundamentals.

Between December 11th and 22nd, Sterling’s movement became erratic as deteriorating UK fundamentals clashed with a fragile US dollar. British labor metrics indicated cooling conditions, with unemployment hitting 5.1% and wage growth moderating to 4.6%, while a sharp drop in November’s CPI to 3.2% solidified the case for BoE easing. However, a slight uptick in the December flash PMI to 52.1 provided enough support for the Pound to defend its recent gains. Concurrently, the greenback struggled as investors prioritized the prospect of an extended Fed easing cycle over robust 4.3% GDP growth. This bearish dollar sentiment was further aggravated by geopolitical unrest fueling a rotation into gold and political commentary questioning the Fed’s future autonomy, which collectively kept the dollar suppressed.

A final push higher developed between December 22nd and 24th, sparked primarily by a fresh wave of dollar selling rather than any internal UK tailwinds. Although final ONS data confirmed a meager 0.1% quarterly expansion for the UK in Q3, traders prioritized an increasingly dovish outlook for US interest rates, propelling GBP/USD further upward into the Christmas break.

Into month-end, trading compressed as liquidity thinned and macro catalysts faded. The Bank of England delivered its December rate cut, lowering Bank Rate to 3.75%, but with the move well priced, sterling largely consolidated near its highs.

AUDUSD

The Australian dollar climbed throughout December 2025, buoyed more by a retreating US dollar than by any significant internal shift in Australia’s fundamentals. The pair began the month on a front foot as fading US rate expectations pressured the greenback, allowing the Aussie to ride a wave of early-month risk appetite. While domestic data provided a steady floor, the figures were more incremental than transformative: third-quarter GDP rose by 0.4% quarterly (reaching 2.1% annually), and October’s household spending climbed 1.3%. Together, these results signaled an economy that, while decelerating, remained resilient as the year drew to a close.

After that initial rise, the pair settled into a protracted phase of choppy, horizontal trading that lasted from December 5th to the 22nd. A dense calendar of economic releases from both Washington and Canberra triggered a constant tug-of-war between buyers and sellers. This influx of competing data points effectively neutralized any momentum, pinning AUD/USD within a restrictive range as market participants lacked the directional conviction to force a breakout.

In Australia, the RBA maintained the cash rate at 3.60% during its December 9 meeting, highlighting a recent “pick up” in inflation alongside strengthening private demand and housing market momentum. This hawkish lean effectively neutralized any expectations for a dovish shift, aligning with an inflation profile that saw headline CPI climb to 3.8% year-over-year in October.

Across the Pacific, the Federal Reserve’s December 10th decision to trim rates by 25bps—bringing the target range down to 3.50%–3.75%—further eroded the dollar’s yield advantage. However, the subsequent market reaction was far from uniform as traders sifted through a series of conflicting economic signals.

A sharp spike in weekly jobless claims to 236k on December 11th initially fueled the bearish dollar narrative, yet this was countered on December 16th by a stronger-than-expected November payrolls print of 64k. While that figure beat the 50k forecast, a simultaneous rise in the unemployment rate to 4.6% and a cooling headline CPI of 2.7% y/y kept the outlook murky. This data cocktail created a classic “push-pull” dynamic: the Aussie found underlying support from its domestic economic resilience, but these gains were frequently checked by the fluctuating and often contradictory expectations for the Fed’s next moves.

A more defined directional shift took hold between December 22nd and 24th, as AUD/USD surged in response to a fresh wave of dollar selling. Investors largely dismissed robust U.S. growth figures—including the 4.3% annualized Q3 GDP print—preferring to focus on the strengthening consensus that the Fed’s easing cycle would persist well into 2026. This downward pressure on the greenback was intensified by simmering geopolitical friction, which saw safe-haven demand pivot toward precious metals rather than the dollar. This environment provided a tailwind for higher-beta currencies, allowing the Aussie to outpace its peers.

As the year drew to a close, AUD/USD entered a period of consolidation, holding onto its recent gains as trading volumes thinned and new macroeconomic drivers disappeared. Ultimately, the pair finished December in a much stronger position; however, this advance was primarily a byproduct of the dollar’s broad-based retreat rather than any significant shift in Australia’s own policy trajectory.

GOLD

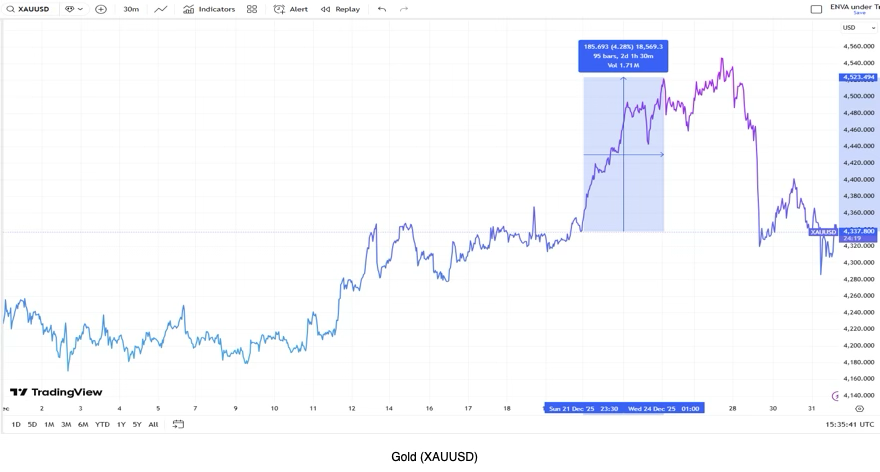

Gold’s trajectory in December 2025 was defined by a shift from cautious range-trading to a historic breakout. The month began with a period of directionless consolidation between December 1st and 11th. While consistent expectations for a Federal Reserve pivot provided a steady floor for prices, any significant upside was checked by intermittent strength in U.S. yields and a resilient dollar ahead of the central bank’s final meeting of the year.

The deadlock was decisively broken between December 11th and 12th. Following the Fed’s 25bp rate cut and an accompanying dovish policy signal, gold prices surged as real yields and the dollar underwent a sharp downward repricing. This shift catalyzed fresh institutional inflows, as investors leaned heavily into the “lower rates, weaker USD” narrative, propelling the metal into a new valuation tier.

Following this spike, gold entered a second phase of consolidation from December 12th to 22nd, though at significantly higher levels. While cooling labor data and slowing inflation prints—highlighted by headline CPI easing to 2.7%—reinforced the disinflationary case, price action remained volatile. Much of the anticipated easing had already been baked into the price, leading to choppy, two-way trade as the market awaited a fresh macroeconomic or geopolitical spark to ignite the next leg of the rally.

A fresh leg of the rally materialized between December 22nd and 24th, as year-end flows magnified gold’s underlying tailwinds. Market attention shifted decisively toward the 2026 outlook, with investors increasingly pricing in a prolonged Fed easing cycle. This dovish sentiment was compounded by a sharp escalation in geopolitical risk—notably following military friction and leadership upheaval in Venezuela—which steered capital away from the dollar and into safe-haven bullion. In an environment of thin holiday liquidity, these factors triggered an outsized move, briefly vaulting gold to a historic intraday peak of $4,549.71 on December 26th.

This month-end volatility peaked on December 29th, when gold prices cratered by approximately 4.5%. This sharp retracement was sparked by a “perfect storm” of year-end factors, most notably a significant hike in margin requirements by the CME Group that forced leveraged traders to liquidate positions. This technical squeeze, combined with aggressive profit-taking following a historic 70% annual rally, was amplified by the thin liquidity typical of the holiday period. The speed of the descent reflected these structural and positioning pressures rather than a fundamental shift in the macroeconomic environment.

By December 30th, the market found its footing as dip-buyers returned to defend key support levels near $4,330. Despite the late-month shakeout, gold concluded the year with a resilient undertone. With the U.S. dollar remaining structurally weak and geopolitical tensions in South America and Eastern Europe still simmering, the metal entered 2026 backed by a supportive macro backdrop and widespread expectations of a move toward the $5,000 milestone.

System Breakdown

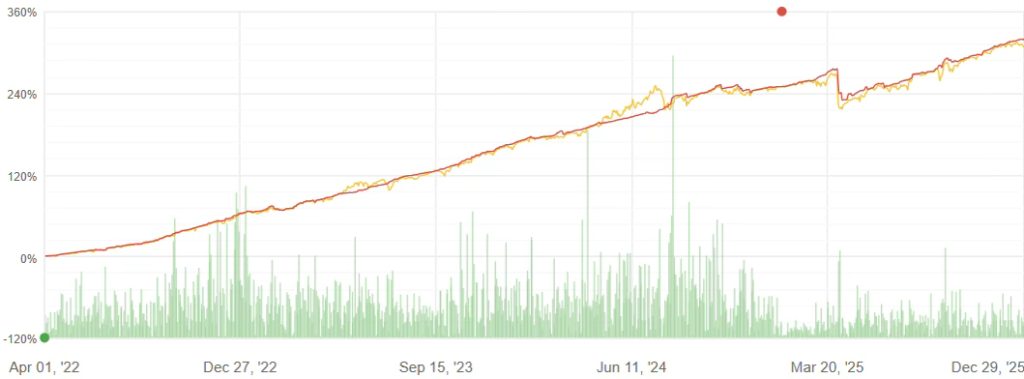

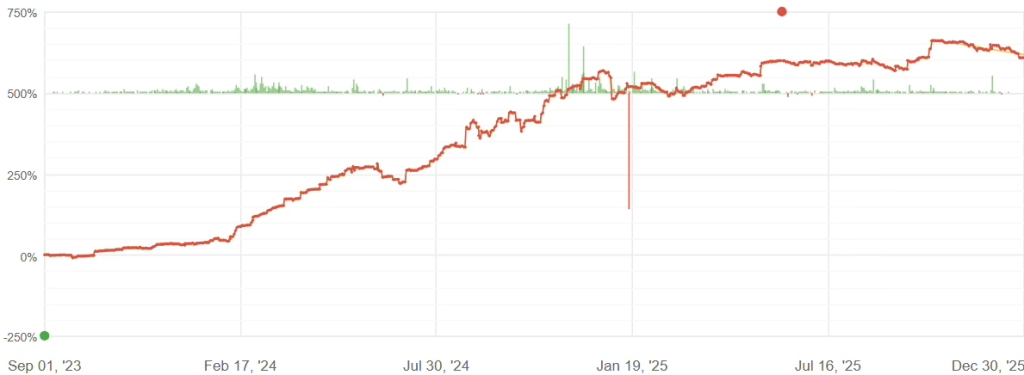

Both R-50 and R-10 finished 2025 with annual returns of 17.8% and 19.7%, respectively, while containing their deepest equity retreats to 13.6% and 14%. Throughout a December characterized by a landmark Fed pivot and a crumbling US dollar, both strategies captured significant upside, posting monthly gains of 3.10% for R-50 and 1.38% for R-10. These systems share a foundational DNA, though R-10 utilizes a specialized trade filter to manage the lower capital requirements of its smaller entry tier.

R-50

Profitability for R-50 was spearheaded by dual-sided trading in Gold, AUDCAD, and NZDCAD, which comfortably offset the minor losses incurred from AUDNZD and CADCHF positions. The market climate in December was particularly suited to Gold and AUDCAD, which together fueled the bulk of the month’s gains. The dramatic repricing of US rates and a spike in safe-haven demand created the exact type of clean, multi-day swings our Gold models are designed to harvest. Simultaneously, the shifting policy gap between Australia and Canada provided reliable volatility that our AUDCAD sub-strategy exploited through both trend-following and mean-reversion entries.

R-10

R-10 saw similar success, with its performance primarily anchored by AUDCAD, EURUSD, and NZDCAD. Activity levels remained high during the period, with R-50 completing 1,222 trades at a 72% success rate and an average duration of two days. R-10 executed 390 trades with a 62% win rate, typically holding positions for a single day.

Following a comprehensive year-end review, we have recalibrated all sub-models to maintain peak efficiency amidst the current global macro shifts. Our commitment to advancing our signal architecture and execution technology remains absolute as we enter 2026, and we are sincerely thankful for the ongoing partnership and confidence of our investors.

R-X25

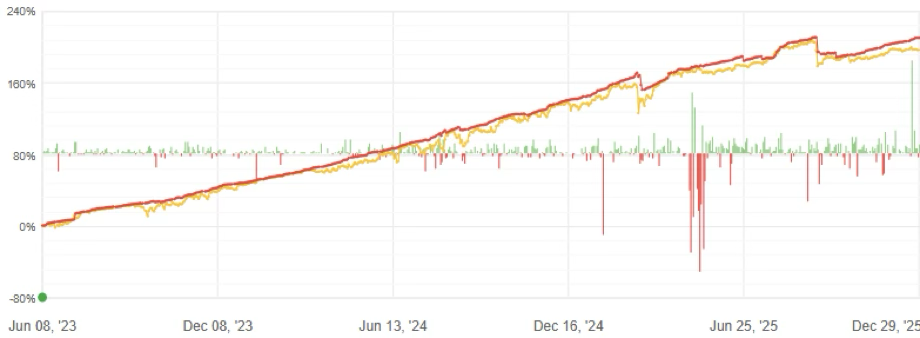

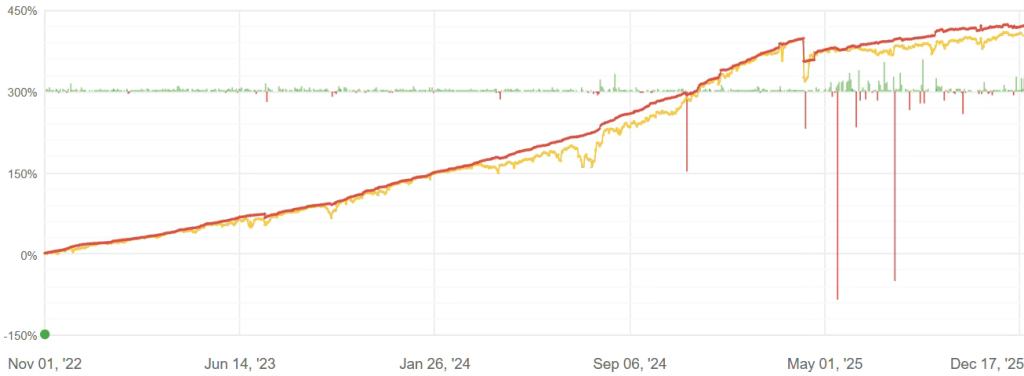

The R-X25 strategy concluded 2025 with an annual return of 27.6% and a maximum drawdown of 15.3%. The combination of evolving Federal Reserve expectations and bouts of volatility across the currency and metal markets created a productive environment for the system, which posted a consistent 2.22% gain in December.

During the month, the strategy completed 561 trades with a 74% success rate and an average duration of two days. The Profit Factor reached a remarkable 4.18, highlighting the system’s high efficiency and precise risk management during a period of fragmented liquidity and changing macroeconomic themes. Performance was primarily fueled by long and short positions in Gold, AUD/USD, and USD/CHF, with no significant losses reported across the portfolio.

Gold acted as a central performance engine, offering sharp fluctuations as the market balanced interest rate repricing and year-end safe-haven flows against technical corrections. This sequence of rapid moves and pullbacks provided the strategy with frequent, high-conviction entries on both sides of the market. Similarly, AUD/USD remained highly responsive to the dollar’s broad retreat and domestic Australian data, creating clear bidirectional setups that fit the system’s multi-day tactical profile. By the close of the year, the strategy maintained active exposure in long Gold, long Euro, and short Gold positions.

Every component of the R-X25 framework underwent a comprehensive recalibration at year-end to align with current market dynamics. We remain dedicated to enhancing our underlying infrastructure and signal processing capabilities. Entering 2026, we lean on a more robust operational foundation and carry strong execution momentum, along with a deep sense of gratitude for the ongoing trust of our investors.

R-C30

The R-C30 strategy finished 2025 with a 10% annual return and a maximum drawdown of 10.1%. Despite its balanced long-short approach to BTC/USD and ETH/USD, the system faced a challenging structural environment in December, closing the month with a 3.48% loss. This underperformance was primarily due to tight trading ranges, frequent price reversals, and a lack of durable directional momentum for the two largest crypto assets.

During the month, the strategy entered 189 trades with an average holding time of four days. This multi-day holding period proved difficult to maintain as established trends failed to gain traction. Both long and short positions acted as headwinds, and no single sub-strategy provided a positive contribution to the monthly P&L.

While BTC/USD edged down 0.85% and ETH/USD gained 2.79% in December, these headline figures obscured the real difficulty for systematic models: both tokens vibrated within inconsistent ranges, where nearly every breakout or breakdown was quickly retraced. This “stop-start” price action penalized directional conviction, as upside moves lacked follow-through and short positions were consistently stopped out by aggressive counter-rallies. By the end of December, the system’s footprint was heavily weighted toward BTC/USD, which represented roughly 72% of total exposure.

At the close of the year, we conducted a rigorous review and recalibration of all subsystems to ensure they remain optimized for the current market regime. Our focus remains on the continuous evolution of our infrastructure, data modeling, and execution logic. We move into 2026 with a strengthened technical framework and a high level of confidence in our execution path, while remaining deeply appreciative of the trust our investors place in us.

R-X5

The R-X5 strategy finished 2025 with an annual return of 18.9% and a maximum drawdown of 8.9%. Throughout a December defined by the Federal Reserve’s pivot, persistent dollar weakness, and inconsistent momentum across the major pairs, the system navigated a constructive yet demanding environment to deliver a monthly gain of 0.63%.

Activity remained precise, with the strategy completing 132 trades at a high 84% success rate and an average holding period of four days. The Profit Factor of 1.76 underscores a disciplined approach to risk capture, maintaining efficiency even as holiday liquidity began to thin. The primary drivers of the month’s performance were long positions in Gold, alongside bidirectional trading in EUR/USD and EUR/JPY, while the only notable drag came from a short position in AUD/NZD.

The system’s Gold strategy was particularly effective, capitalizing on the “lower rates, weaker USD” narrative that propelled the metal higher as real yields compressed. These sustained upside phases aligned perfectly with the system’s multi-day tactical profile. EUR/USD also yielded high-quality results; as the pair oscillated between the Fed’s easing signals and a more cautious ECB, the strategy successfully harvested gains from the resulting range-bound but volatile structure. By the end of the year, the portfolio’s exposure was primarily concentrated in EUR/USD shorts and a balanced long/short stance on AUD/CAD.

Following our standard year-end protocol, all subsystems were rigorously reviewed and recalibrated to ensure they remain optimized for the shifting macro landscape. We continue to invest in our infrastructure and signal generation to refine every aspect of the execution process. As we enter 2026, we do so with a resilient framework and sincere gratitude for the continued confidence our investors have placed in us.