Overview

The year 2025 was marked by unprecedented market volatility. Although many hedge funds and traditional trading systems failed to adapt, our technology demonstrated impressive resilience. Beyond simply protecting capital, our systems successfully generated robust net profits by the close of the year.

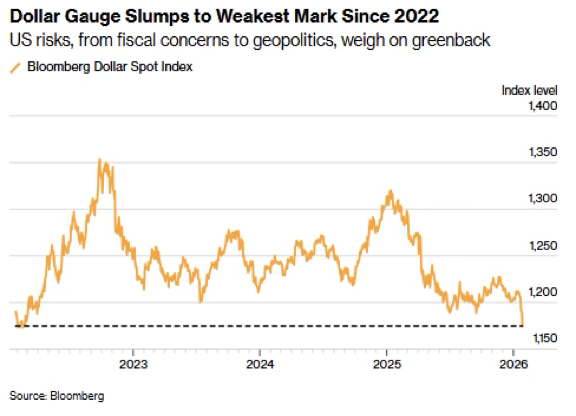

The opening month of the year was defined by profound instability, mirroring the market disruptions seen after last year’s Liberation Day. As global investors navigated a landscape of decelerating growth, diplomatic friction, and skepticism toward central bank strategies, the United States became the focal point of this volatility. Growing domestic political discourse and trade-related anxieties began to tarnish the dollar’s reputation as a secure asset, fostering a “Sell America” trend that triggered substantial revaluations in both forex and commodity markets.

Initially, the greenback maintained a slight upward trajectory through the first week of January, fueled by a cautious market environment and expectations that the Federal Reserve would maintain current interest rates. During the period of January 1–5, the US Dollar Index (DXY) climbed above 98.50, a move prompted largely by escalating tensions with Venezuela rather than domestic economic indicators. However, this early strength proved unsustainable; by mid-month, concerns regarding geopolitical stability and policy transparency overrode the support from interest rate differentials, leading to a sharp reversal as market participants pivoted toward a broader diversification strategy away from US-denominated assets.

From 6–10 January, the dollar’s upward momentum expanded slightly as domestic employment figures indicated a slowing, yet still stable, labor market. Specifically, the 208k initial jobless claims filed for the week concluding January 3 arrived just under forecasted levels, signaling resilience despite broader economic moderation.

In tandem, the ADP report indicated a private-sector employment increase of 41k for December, trailing the anticipated 47k, while JOLTS job openings dipped to 7.146m against a projected 7.6m. These figures align with a broader trend of a decelerating labor market that, despite the cooling demand, is not experiencing a sudden or severe collapse.

The government’s employment data confirmed this trend, with December’s non-farm payrolls increasing by 50k, falling short of the 60k projection. Simultaneously, the unemployment rate saw a marginal decline to 4.4%. Taken together, these metrics illustrate a labor sector that is evidently losing steam without signaling an immediate economic collapse.

This data combination served to steady interest rate forecasts, as investors maintained a strong conviction that the Federal Reserve would hold rates steady during its January meeting. This environment provided enough support for the dollar to continue its gradual ascent toward the 99.00 threshold.

During the period of 10–16 January, the dollar held steady near its monthly peaks, bolstered by robust economic activity and inflation figures that justified a cautious approach to interest rate adjustments. A 0.6% monthly increase in retail sales exceeded forecasts, while producer prices also outpaced expectations, with both headline and core PPI reaching 3.0% on an annual basis. These results reduced the likelihood of near-term rate cuts and propelled the DXY into a brief trading range of 99.10–99.15. Nevertheless, further appreciation was restricted by ongoing skepticism regarding the Federal Reserve’s autonomy and the overall transparency of monetary policy.

After January 16, the market sentiment underwent a fundamental change, initiating a significant downward turn in the dollar’s value.

Between 16 and 21 January, the dollar faced mounting headwinds as geopolitical shifts began to dominate market sentiment. Growing friction between the US and Europe regarding Greenland, paired with renewed tariff threats, disturbed investors and fueled anxieties over the stability of long-term diplomatic and commercial ties. This resulted in a clear shift in foreign exchange markets: rather than viewing these tensions as temporary risks that bolster the dollar’s safety, investors increasingly saw them as fundamental flaws necessitating a move away from US-denominated holdings. Simultaneously, fresh debate concerning the Federal Reserve’s autonomy and future policy direction left the currency more exposed, pulling the DXY back under the 99.00 level.

The sell-off gained momentum from 21 to 27 January as confidence in the long-term attractiveness of US assets wavered. The DXY dropped toward 97.00, reaching its lowest point in several months, as the combination of policy ambiguity, international disputes, and capital outflows toward other currencies outweighed any stability provided by US interest rates. Even with expectations that the Fed would maintain its current stance at the January meeting, this support proved too weak to halt the broader market correction.

The most intense period of depreciation occurred surrounding the Fed’s 28 January announcement. Despite the decision to keep rates between 3.50% and 3.75%, the dollar continued to slide as political comments suggested a preference for a weaker exchange rate, reinforcing the “Sell America” trend. A sharp sell-off followed President Trump’s dismissal of the currency’s decline; however, the more lasting impact was the market’s perception of a quiet acceptance of further dollar weakness. Consequently, the DXY recorded its most severe single-day loss in months—falling as much as 1.2%—while capital surged toward alternative hedges, particularly gold.

This trend saw a partial reversal on 30 January, as the dollar achieved its most significant rally since mid-2025 following the nomination of Kevin Warsh as Federal Reserve Chair. Because Warsh is perceived as an inflation hawk who might resist extensive rate reductions, his selection disrupted the ongoing currency debasement theme, triggering a widespread dollar recovery and a sharp sell-off in precious metals. Although this late-month bounce reduced the dollar’s total losses, the DXY still ended January with a decline of approximately 1.4%, albeit with a more stabilized risk profile.

This unusual environment led to unconventional price action among major pairs, where AUDCAD, NZDCAD, Gold, and AUDUSD became the primary performance drivers, overshadowing traditionally dominant market pairs.

Specifically, AUDCAD progressed through three clear stages in January: an initial rally, a middle period of price stabilization, and a significant surge toward the end of the month that established new peaks before a minor retracement at the close.

Between 1 and 7 January, AUDCAD rose consistently, gaining roughly 2% by the end of the first week. This appreciation was fueled by the Australian dollar’s relative strength against a Canadian dollar burdened by sluggish domestic economic data and global uncertainty. This initial phase was characterized by steady, controlled gains, which established the foundation for the consolidation period that ensued.

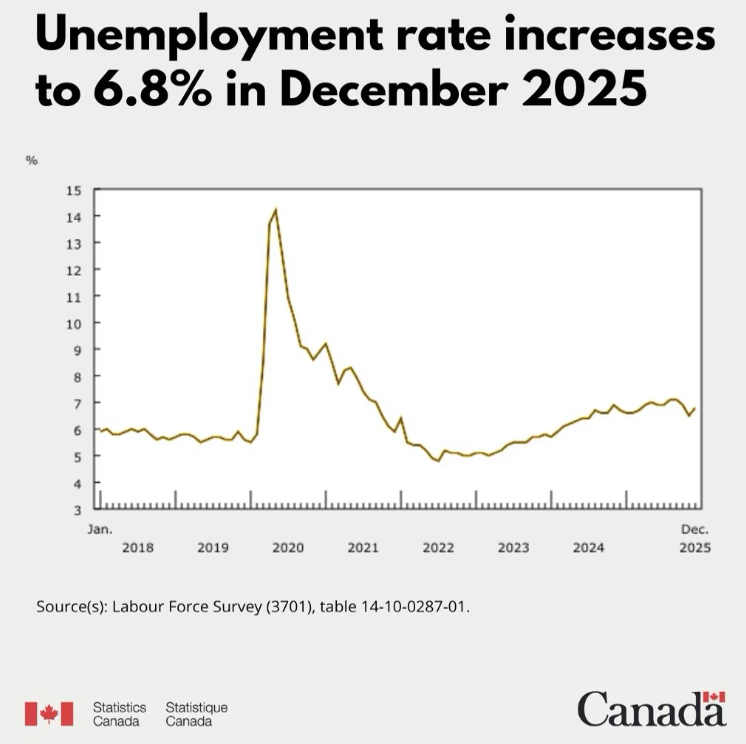

From 7 to 21 January, the pair moved horizontally within a narrow corridor, as upward momentum stalled and selling pressure found immediate support. Inconsistent economic reports from both nations prevented a clear directional bias. In Australia, the November monthly CPI figure of 3.4% year-over-year came in below the 3.6% forecast on 6 January, momentarily cooling expectations for a more aggressive Reserve Bank of Australia. Meanwhile, Canada’s December employment data released on 9 January reported a gain of 8.2k jobs alongside an increase in the unemployment rate to 6.8%, suggesting that while hiring remains positive, the overall labor market is loosening. This equilibrium between the two currencies maintained the AUDCAD within its established range through the middle of the month.

Market sentiment underwent a slight adjustment around 19–20 January following an unexpected headline inflation reading in Canada, where December CPI climbed to 2.4% year-over-year against a 2.2% forecast. However, because core inflation metrics continued to moderate, the Canadian dollar failed to sustain any meaningful momentum, leaving AUDCAD within its existing trading range.

The pair finally broke out of its consolidation phase after 21 January, embarking on a steep upward climb. This shift was triggered by Australia’s December employment report, which significantly outpaced projections as the jobless rate dropped to 4.1% and 65.2k jobs were added. This rally found further support following the 28 January release of Australia’s December CPI, which accelerated to 3.8% from the previous 3.4%, strengthening the argument for future monetary tightening.

Conversely, the Bank of Canada offered no significant resistance to this move. During its 28 January meeting, the bank maintained interest rates at 2.25%, citing high levels of uncertainty—specifically regarding trade—rather than adopting a more restrictive stance. This lack of hawkishness left the Canadian dollar vulnerable while the Australian dollar’s momentum intensified.

Despite a robust Canadian retail sales report for November—showing a 1.3% monthly increase on January 23—the combination of a loosening job market and the Bank of Canada’s wary outlook prevented the CAD from keeping pace with the late-January surge in the AUD. Consequently, AUDCAD finished the month with an overall gain exceeding 3.55%, settling near 0.948 after momentarily peaking just below its monthly high.

Similarly, NZDCAD trended upward throughout January, characterized by initial growth followed by a volatile mid-month plateau and a final, aggressive rally toward the close. This trajectory was primarily driven by an expanding gap in the economic performance and monetary policy outlooks of New Zealand and Canada, a divergence that intensified as the month went on.

The pair began the year with positive momentum, advancing during the first week as the NZD benefited from a stabilization in global economic sentiment. Meanwhile, the CAD was weighed down by indicators of domestic economic underperformance. These early gains were measured, pushing NZDCAD to a roughly 1% increase by the start of the month.

Upward movement paused during the middle of January, leaving NZDCAD to trade horizontally despite increased daily volatility. Canada’s December employment figures, published on 9 January, illustrated this environment: while 8.2k jobs were added, the jobless rate rose to 6.8% due to higher labor force participation. This data suggested a steady increase in economic slack rather than a sudden crash, a factor that cushioned the Canadian dollar against sharp declines but failed to provide a foundation for a lasting rally.

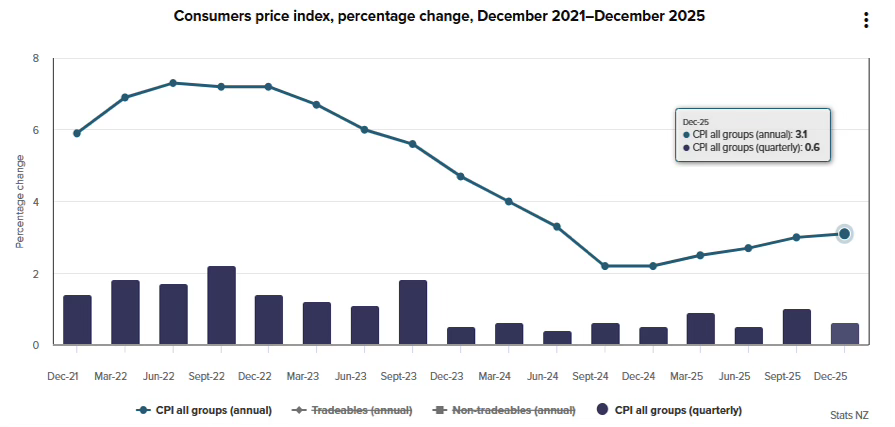

The market dynamic changed significantly during the latter half of the month following higher-than-anticipated inflation data from New Zealand. The fourth-quarter CPI, published on January 22, showed a quarterly increase of 0.6% and an annual rise of 3.1%. This shift pushed inflation back above the Reserve Bank of New Zealand’s 1–3% target range, leading investors to dismiss the likelihood of additional rate cuts after the Official Cash Rate was lowered to 2.25% at the end of the previous year.

In contrast, Canadian inflation trends provided less momentum for the currency. Although the headline CPI rose to 2.4% year-over-year in December—surpassing the 2.2% forecast on January 19—core inflation metrics remained on a downward path, strengthening the belief that interest rates would stay unchanged.

Toward the end of the month, New Zealand’s trade performance provided an additional boost. The trade balance for December moved into a surplus of NZ$52 million, supported by NZ$7.7 billion in exports against NZ$7.6 billion in imports. Meanwhile, the Bank of Canada opted to maintain its policy rate at 2.25% on January 28, further highlighting the divergence between the two economies.

As the New Zealand dollar found firmer footing and the Canadian dollar lacked any significant momentum, NZDCAD surged toward the end of the month, finishing January with an overall gain of approximately 3.75% following a short period of stabilization at those higher prices.

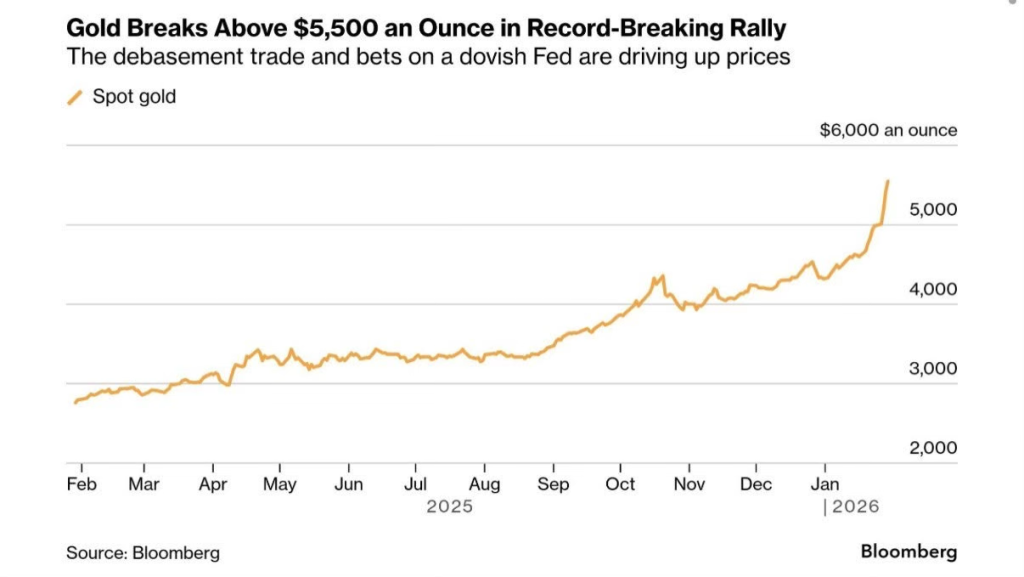

Gold maintained an upward trajectory throughout January, beginning with a gradual climb before transitioning into a major late-month rally that shifted the market environment. The first two weeks saw consistent buying as investors factored in anticipated rate cuts and rising policy risks. However, the latter half of the month evolved into a high-conviction trade, with gold prices rising sharply as market participants looked for a hedge against currency instability and sovereign risk.

From January 1 to 16, gold trended higher in a measured ascent, supported by a gradual cooling in US inflation and a steady drift lower in confidence around policy direction. The key US inflation print on January 13 was broadly consistent with disinflation continuing, reinforcing expectations that the Fed could remain in a prolonged pause after cutting rates three times in late 2025, allowing gold to grind higher.

That steady climb shifted into a sharp breakout after mid-month as geopolitical and credibility risks intensified and the dollar began to lose its traditional safe-haven monopoly. Tensions around US trade posture—most visibly the Greenland-related tariff threats against European nations—reignited Sell America positioning and broadened demand for non-fiat stores of value. By January 26, gold pushed above $5,000 per ounce for the first time, reaching a peak of approximately $5,595 by January 29. This reflected a rapid repricing of risk premia rather than any single data catalyst.

However, the vertical rally met a sudden end on January 30. The nomination of Kevin Warsh as the next Federal Reserve Chair introduced a significant shift in market expectations, with investors viewing him as a credible figure who might prioritize a smaller balance sheet and a firmer stance on the 3% inflation floor. This sparked a massive liquidity event and a sharp reversal in crowded long positions, causing gold to tumble nearly 10% in a single session and ending the month back below the $5,000 mark.

The most aggressive gains occurred between 27 and 29 January, as gold reached a series of record peaks. This surge was fueled by investors perceiving US political commentary and policy ambiguity as a sign of acceptance for continued dollar depreciation. Prices climbed past $5,400 per ounce, a move deeply connected to the currency debasement theme and a widespread exit from fiat currencies and government debt. The Federal Reserve’s 28 January announcement to maintain rates between 3.50% and 3.75% failed to dampen the momentum, as the rally was steered by a fundamental loss of confidence and a rush for hedges rather than immediate interest rate gaps. This upward trend briefly continued into the end of the month, with gold hitting levels near $5,580 per ounce during early Asian trading sessions.

The month-end saw an abrupt reversal in momentum. Gold underwent a steep downward repricing after President Trump nominated Kevin Warsh for Fed Chair—seen as a more inflation-focused choice—and US inflation data came in firm, causing a sharp unwinding of easing hopes. Prices plunged nearly 10% on January 30, momentarily dipping under $4,900/oz and stripping away much of the late-month progress. Even though gold finished January up overall, this aggressive retreat showed how quickly confidence-led rallies can break when policy expectations shift.

AUDUSD followed a two-part story in January: an initial jump that dissolved into mid-month softness, succeeded by a vigorous recovery that left the pair significantly higher by the close.

Between 5 and 7 January, AUDUSD climbed in a steady fashion as a slightly positive risk environment and waning USD rate dominance provided support. However, these gains were temporary. From 7 to 16 January, the pair retraced the entire move and trended downward as US economic figures suggested a gradual cooling rather than a collapse, sustaining dollar demand. The 9 January payrolls report, which showed a 50k job increase and a 4.4% unemployment rate, indicated sluggish hiring that was still insufficient to trigger a sudden change in Fed policy.

Mid-month marked a turning point, with the momentum shifting decisively in the Aussie’s favor from 18 January. Domestically, the December labor force data released on 22 January delivered a major upside surprise: 65.2k jobs were added—the vast majority being full-time positions—while unemployment dipped to 4.1%. This robustness suggested a labor market tight enough to warrant a continued hawkish stance from the RBA.

Meanwhile, US inflation figures offered a mixed bag. While December’s CPI (released 13 January) showed a steady but slow cooling—rising 0.3% monthly and 2.7% annually—it wasn’t the definitive “mission accomplished” signal markets were hoping for. While this data initially kept AUDUSD gains in check, the landscape changed abruptly in late January as the US dollar began to buckle under renewed pressure.

The final push in late January was fueled by an increasing split in inflation and policy paths. Australia’s CPI data on 28 January showed a rise to 3.8% year-over-year, confirming that price pressures were still persistent and likely to keep the RBA on a restrictive path. Conversely, the US dollar faltered as political distractions and policy doubts took center stage, even after the Fed kept rates between 3.50% and 3.75%. This environment cleared the way for AUDUSD to surge, reaching a three-year peak toward the end of the month.

This momentum partially faded on 30 January, with AUDUSD retreating toward 0.7000 as the US dollar bounced back. The recovery followed President Trump’s nomination of Kevin Warsh as Fed Chair, a move that restored market faith in central bank independence and countered the sell-dollar trend. Strength was added by firmer US producer price data, with headline PPI hitting 3.0% and core at 3.3%, while Australia’s quarterly PPI remained flat at 3.5%, indicating steady domestic price pressure. Despite the pullback, markets still factored in over a 70% chance of an RBA rate hike, implying the dip was driven by dollar rebalancing rather than a loss of support for the Aussie.

The Path Ahead

As we move into a new cycle, 2026 is poised to be another record-breaking year for the global markets. We continue to lead the sector through our advanced preparation and the ongoing evolution of our technology.