Macroeconomic & Market Overview

Throughout June, the US Federal Reserve abandoned its cautious hedging strategy. Confronted by persistent inflation running well above target levels and a continuously robust domestic employment landscape, alongside falling crude prices resulting from a diplomatic agreement between the US and Iran, the central bank adopted a decisively aggressive posture during its June gathering. This major policy shift upended currency markets worldwide, significantly strengthening the greenback, squeezing interest-rate-sensitive currencies, and sparking a widespread liquidation of asset classes that had previously thrived on market volatility. The American currency served as the absolute epicenter of these global market adjustments.

At the start of the month, the US Dollar Index (DXY) traded closely around the 99.00 threshold. It was caught in a tug-of-war between safe-haven flows tied to stalled US-Iran diplomatic negotiations and escalating domestic inflation anxieties fueled by fresh tariff proposals emerging from Washington.

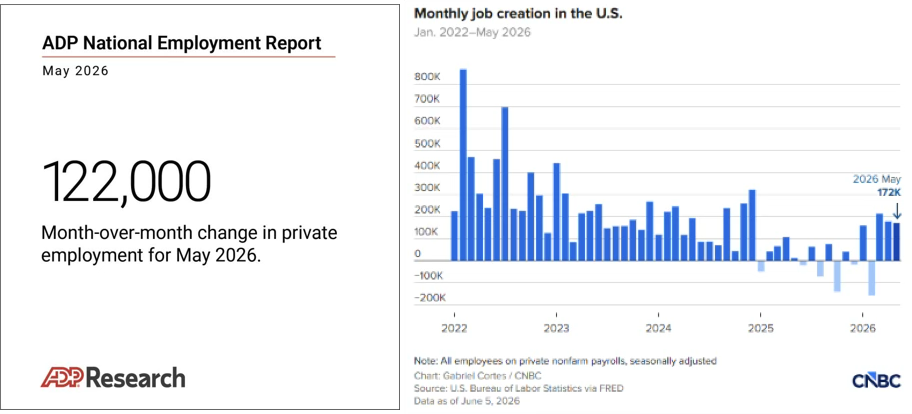

Macroeconomic indicators early on strongly supported an aggressive monetary policy stance. The ADP employment report exceeded expectations with 122,000 new jobs against the projected 117,000. This was immediately followed on June 5 by a massive Non-Farm Payrolls (NFP) surprise, which printed at 172,000 positions versus an anticipated consensus of 85,000. Consequently, the implied probability of a Federal Reserve rate increase by December surged to 81%, driving a steady appreciation of the greenback over the opening week and pushing a key psychological resistance point near 100.00 into view.

Beginning June 8, the greenback paused its rally and entered a consolidation phase, rather than extending higher. Investors paused to await incoming inflation metrics to determine if the aggressive rate repricing was fundamentally justified. Because the Federal Reserve had entered its official pre-meeting quiet period, market participants received no tempering or dovish remarks to challenge the expectation of tighter credit conditions.

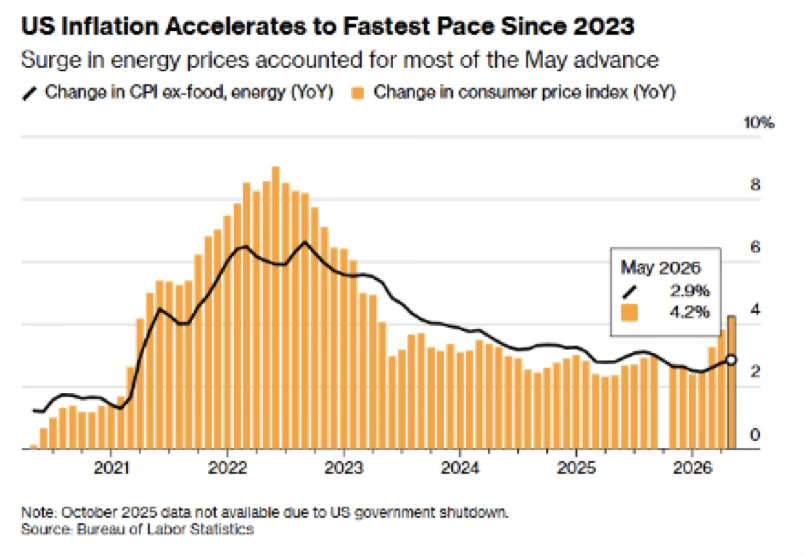

The Consumer Price Index (CPI) report published on June 10 presented conflicting signals: year-on-year headline inflation climbed to 4.2% (outpacing April’s 3.8% and matching forecasts), whereas the monthly core metric arrived unexpectedly soft at 0.2%. However, the Producer Price Index (PPI) released the next day reinforced broader inflationary worries, revealing that final demand jumped by 1.1% month-on-month, significantly beating the 0.7% projection. Amid these dynamics, the DXY remained bound within its recent range leading up to the FOMC gathering, with investors awaiting specific policy direction from Fed official Warsh.

The tone of the entire month shifted dramatically following the June 17 Federal Reserve session. Although policymakers voted unanimously to leave the benchmark interest rate unchanged at 3.50%–3.75%, the accompanying guidance was decisively aggressive. The median interest rate forecast (dot plot) for 2026 was adjusted upward to 3.8% from the 3.4% projected back in March. Furthermore, nine out of the eighteen committee participants now anticipated at least one rate hike before the year concludes. Crucially, the central bank completely eliminated its previous easing bias from the official policy statement, replacing it with an explicit commitment to combatting inflation and ensuring price stability.

Immediately following the announcement, the greenback broke through the 100.00 mark, continuing its upward trajectory to reach 101.00 within 48 hours-marking its sharpest two-day rally in a quarter. By June 22, the CME FedWatch tool indicated that the likelihood of at least two interest rate increases in 2026 had spiked to 58.5%, a massive jump from the 17.1% recorded just a week prior.

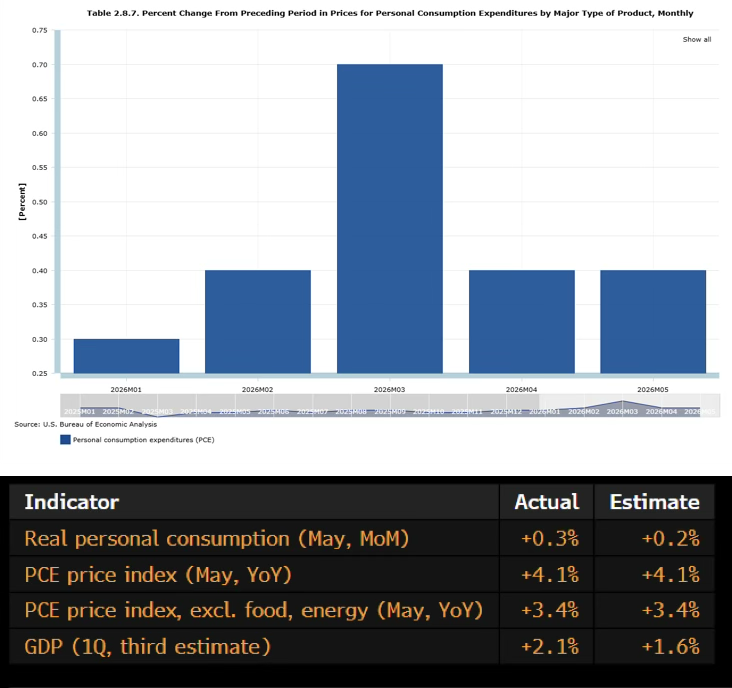

During the final stretch of June, the upward momentum slowed down, though the currency did not experience a significant pullback. The release of May’s Personal Consumption Expenditures (PCE) data on June 25 verified that price pressures remained entrenched, showing headline and core figures at 4.1% and 3.4% year-on-year respectively, aligning perfectly with consensus estimates. Nevertheless, the month-on-month reading of 0.4% fell slightly short of the 0.5% forecast, which prompted market participants to modestly dial back their rate-hike expectations. According to CME FedWatch data, the probability of a July rate hike softened from 34.2% to 28.9%, while the likelihood of a September increase eased from 65.7% to 60.1%. This caused the greenback to pull back slightly from its peak as the month concluded.

Despite the late-month softening, the US dollar concluded June with substantial net gains. This strength was underpinned by a decisive shift toward tighter monetary policy and a durable widening of interest rate differentials in favor of the US. Investors are now focused on the upcoming July FOMC gathering and subsequent inflation data releases to guide the next major trend. In this macroeconomic environment, rate-sensitive and commodity-dependent currencies bore the primary burden of the greenback’s appreciation.

Foreign Exchange & Asset Deep-Dives

AUD/USD Currency Cross

The AUD/USD currency pair faced persistent downward pressure throughout June. Rather than being driven by domestic economic factors, the pair’s movement was primarily dictated by the expanding monetary policy mismatch between an increasingly aggressive Federal Reserve and a Reserve Bank of Australia (RBA) that had chosen to pause its cycle. The cross initiated the month around 0.7200 and steadily depreciated during the opening week. This drop was accelerated by blockbuster US employment data (the NFP expanding by 172k versus an 85k estimate), which bolstered expectations for higher US interest rates and redirected capital flows toward the greenback.

Mid-month brought a brief corrective bounce that lifted AUD/USD back toward 0.7080. This recovery was partly fueled by the June 16 release of the RBA’s meeting minutes, which revealed that policymakers had debated implementing another rate increase before deciding on a pause, thereby hinting that the tightening cycle might not be over. However, this rebound was short-lived. The aggressive FOMC statement on June 17 triggered the sharpest downward leg for the pair, sending AUD/USD plunging below 0.7000 within two trading sessions as yield differentials shifted firmly and structurally in favor of the US dollar.

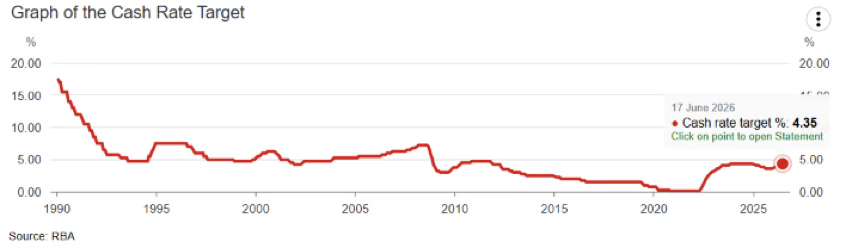

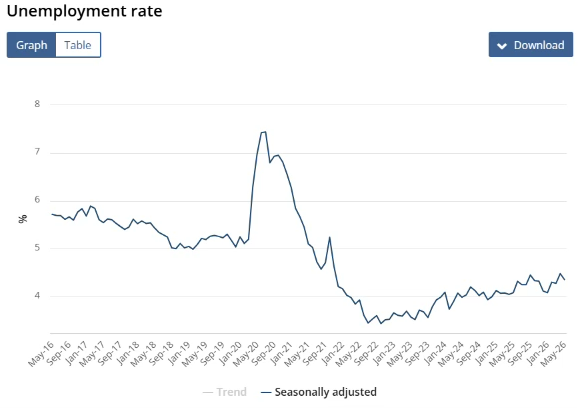

The RBA’s subsequent policy announcement on June 24 to maintain its benchmark rate at 4.35% provided no support for the Australian currency. This unanimous decision to pause matched consensus forecasts perfectly; though officials noted that inflation remained uncomfortably high and left the door open for future rate hikes, investors interpreted the move as confirmation that the RBA had entered a passive, observational stance just as the Fed was actively shifting to a highly aggressive posture. Even an exceptionally strong domestic labor report on June 25-showing an addition of 40,300 jobs against a forecasted 30,000, along with a drop in unemployment to 4.4%-offered only temporary stability and failed to alter the broader trend.

Ultimately, the Australian dollar finished June deeply in negative territory, its weakness reflecting a macroeconomic landscape that favored the greenback.

USD/CAD Currency Cross

The USD/CAD currency pair climbed steadily during June, driven by a widening interest rate and policy mismatch between the two neighboring economies.

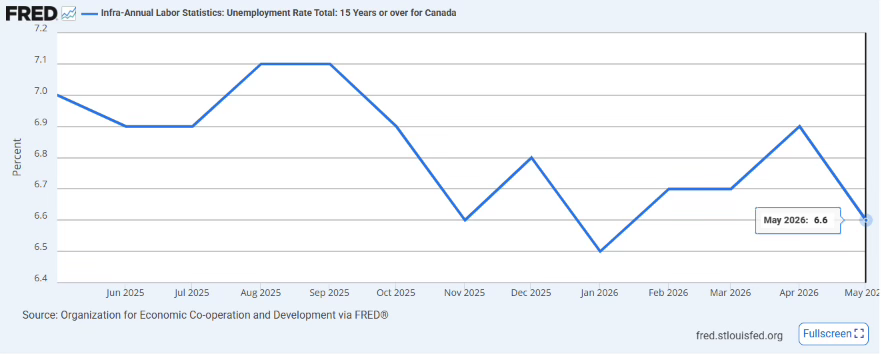

Starting the month near 1.3800, the pair registered steady gains over the first week, propelled by broad greenback strength and a Canadian employment release on June 5. Although the Canadian jobs data appeared exceptionally robust on the surface-adding 88,000 positions versus a modest 10,000 forecast, and lowering unemployment from 6.9% to 6.6%-it failed to shift market expectations that the Bank of Canada (BoC) would remain passive. The BoC validated this outlook on June 10 by holding its policy rate steady at 2.25% for the fifth consecutive time, noting that the domestic economy faced headwinds and was dealing with excess supply.

With the Federal Reserve holding its target rate at 3.50%–3.75% and signaling subsequent increases, the yield gap stood at 125 basis points-and was positioned to widen even further. The aggressive FOMC outcome on June 17 sparked the pair’s most dramatic upward surge, pushing USD/CAD above 1.4100 and extending its gains toward 1.4200 within a two-day window. May’s Canadian CPI data, published on June 22, introduced further complexity by showing headline inflation accelerating to 3.2% (above the 3.0% projection) due to a 33.2% spike in retail gasoline costs. However, because the BoC’s preferred core inflation metrics remained steady near 2.0%, the data supported the central bank’s stance to discount this temporary energy shock.

Consequently, the Canadian dollar ended June in a weakened position, hampered by a domestic central bank maintaining interest rates far below those of the US, alongside an economy facing ongoing US tariff ambiguities and elevated energy inputs.

GBP/USD Currency Cross

The British pound followed an unstable path against the dollar during the first two weeks of June. The pair tumbled sharply on June 5, driven by the blockbuster US NFP print (172k jobs versus an 85k consensus) that sparked broad dollar buying and forced sterling back down toward the 1.3300 level. Subsequently, the pair managed to claw back its losses, lifting gradually as geopolitical anxieties regarding Iran subsided ahead of consecutive major UK economic events: the June 17 inflation release and the June 18 Bank of England (BoE) policy decision.

The CPI figures provided initial optimism, with headline inflation holding steady at 2.8% year-on-year, undershooting the 3.0% expectation. However, the underlying details painted a more problematic picture: services inflation-the metric most heavily prioritized by the BoE-surged from 3.2% in April to 3.7%. The central bank explicitly cautioned that headline CPI would likely climb toward 3.25% in the final quarter of the year as energy costs continued to manifest across the economy. The following day, the BoE kept its key interest rate at 3.75% in a 7-2 vote. While the hawkish minority advocating for an immediate rate increase doubled compared to April, the overall outcome failed to provide sterling with a sustainable upward catalyst.

Subsequent movements were directed almost entirely by developments across the Atlantic. The aggressive Federal Reserve pivot on June 17 catalyzed the sharpest drop of the month for GBP/USD, forcing the pair lower over two days and breaching the key 1.3200 floor. This downward pressure was further aggravated on June 22 by the sudden resignation of Prime Minister Starmer, which introduced a layer of political instability that choked off any meaningful recovery attempts. Sterling concluded the month with notable losses, weighed down by an aggressive Fed, sluggish domestic economic expansion, and sticky services inflation that severely constrained the Bank of England’s policy options.

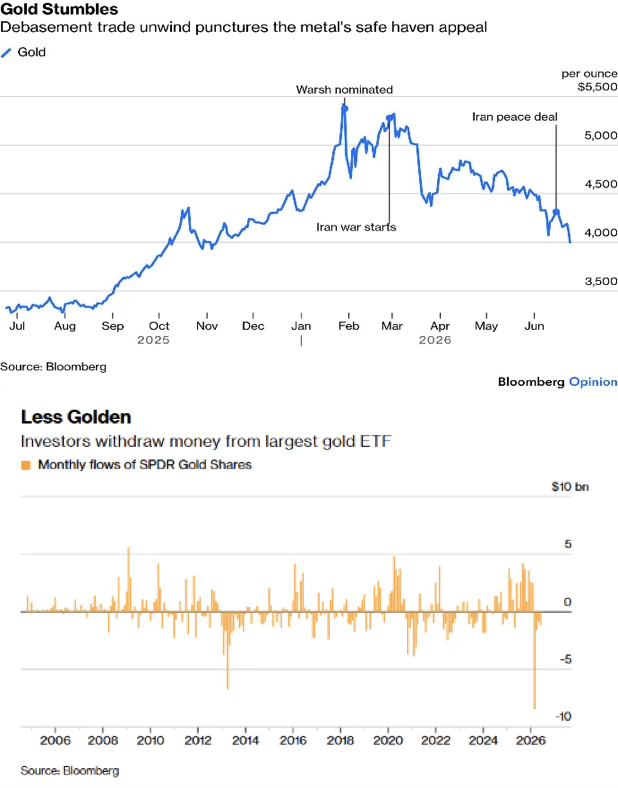

Gold (XAU/USD)

Gold faced negative headwinds entering June, continuing a retreat from its record March peaks as geopolitical risk premiums gradually dissipated. This downward trajectory accelerated during the first half of the month, as a resurgent dollar and spiking US interest rate expectations-triggered by the strong June 5 NFP employment beat-dragged bullion below $4,300 per ounce. This decline reflected the mounting opportunity cost of holding a non-yielding asset as US government bond yields climbed.

A temporary mid-month correction lifted the precious metal back toward $4,375, supported by the official confirmation of a peace agreement between the US and Iran and the anticipated reopening of the Strait of Hormuz, which together stripped away the energy-driven inflation premium previously priced into the market. However, the June 17 FOMC outcome dealt a decisive blow. The Fed’s aggressive dot plot projection impacted the metal through two separate channels: climbing real interest rates increased the cost of carrying non-interest-bearing bullion, while a strengthening greenback made gold significantly more expensive for foreign buyers. As a result, gold plummeted to near $3,975, marking its lowest valuation since early in the year.

The structural backdrop proved equally unfavorable. The prevailing “debasement trade” thesis-which argued that a weak US dollar and runaway fiscal deficits would continuously erode purchasing power and sustain gold’s multi-year rally-rapidly dissolved as the Federal Reserve demonstrated its commitment to monetary tightening. This shift in sentiment was backed up by capital flows: nearly $1 billion was pulled from the SPDR Gold Shares ETF during June alone, pushing total outflows since the end of February to $12 billion-the most significant four-month capital flight from the fund since 2013.

Gold stabilized around $4,000 as the month drew to a close, with the US-Iran peace accord helping it recover slightly from its absolute lows, though this was insufficient to reverse a month defined by escalating real yields, a powerful dollar, and the large-scale liquidation of a thematic trade that had pushed the asset to historic highs just months before.