Overview

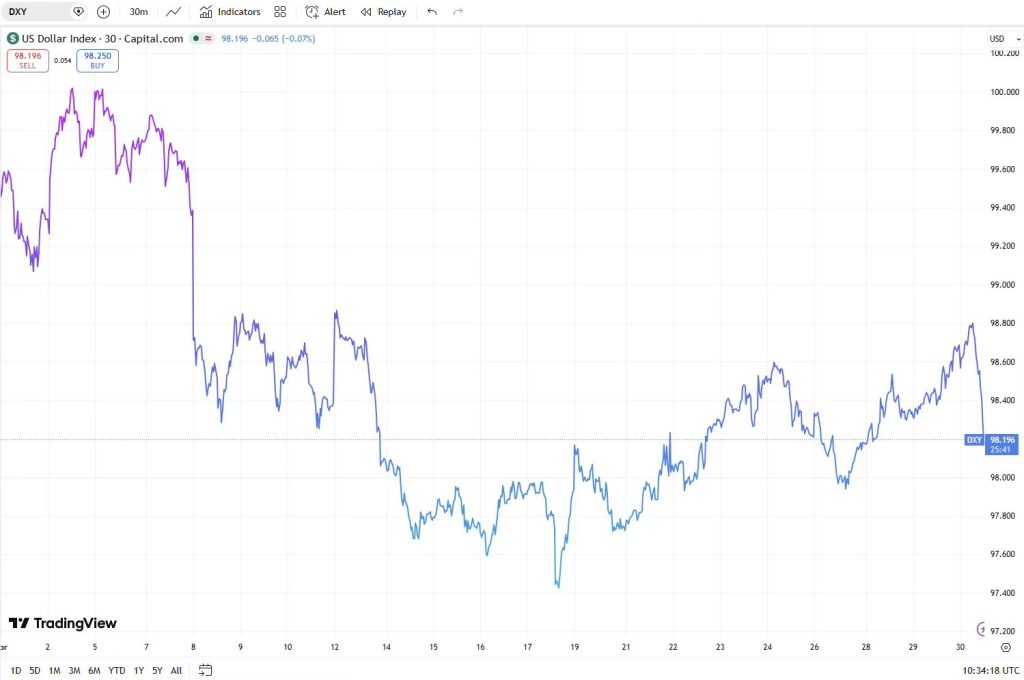

The landscape throughout April 2026 was primarily defined by geopolitical tensions as the ongoing confrontation between the United States and Iran entered its second month. This prolonged instability left energy sectors in a state of high alert and caused inflation projections to fluctuate wildly, which effectively forced the Federal Reserve to maintain a passive stance. The continued blockade of the Strait of Hormuz, coupled with the recurring cycle of emerging and collapsing ceasefire prospects, caused crude prices to react sharply to every diplomatic development. Consequently, the currency markets remained tethered to these shifts, with the greenback dominating the narrative and dictating the movement of all other assets.

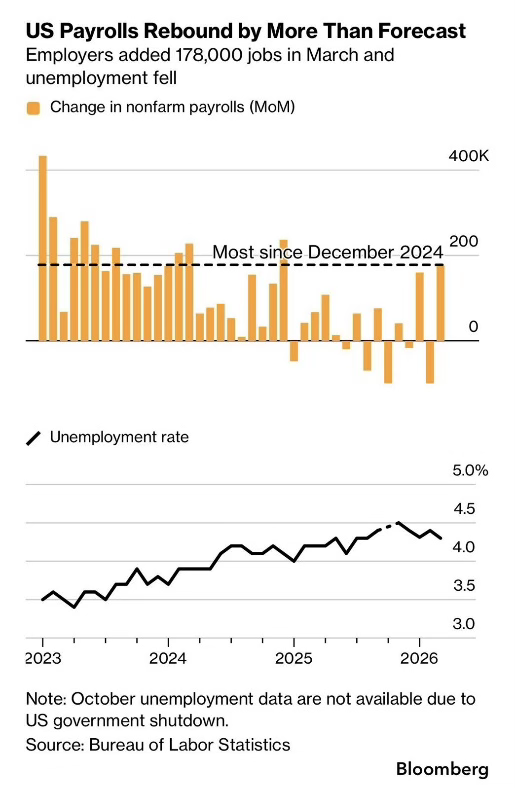

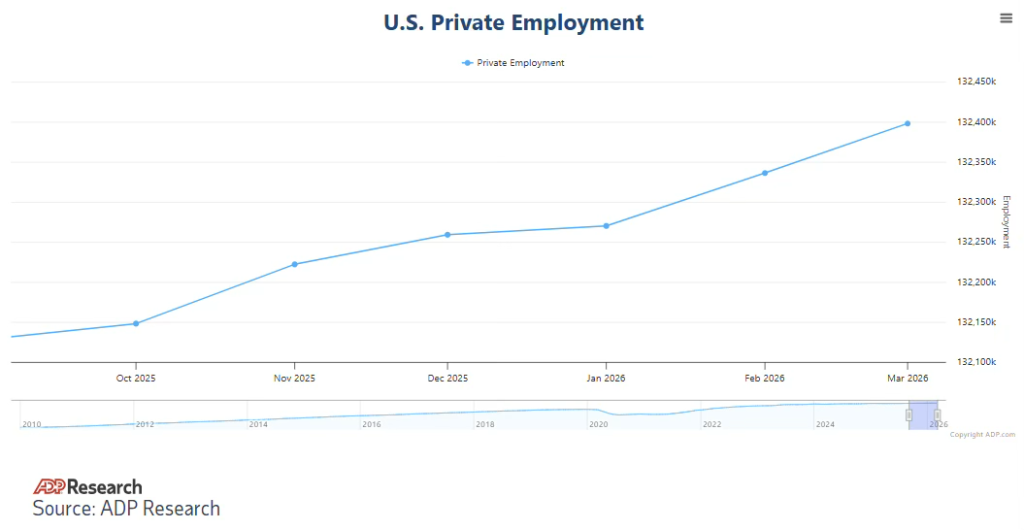

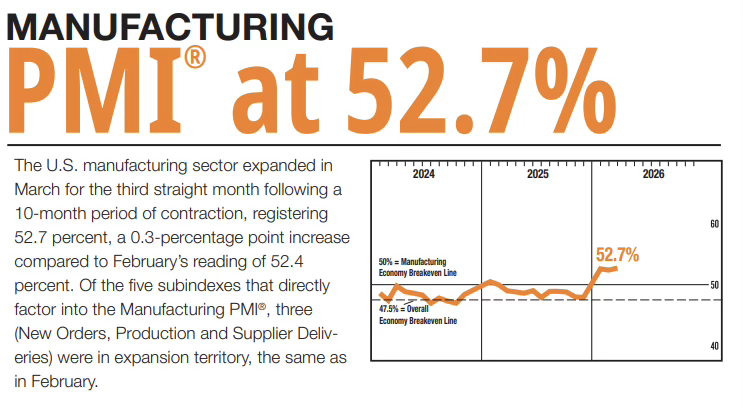

The American currency started the month with significant upward momentum, seeing the DXY index approach the 100.00 threshold during the initial two trading days. This strength was underpinned by robust economic data, including a March non-farm payroll report that reached 178,000 positions—far exceeding the anticipated 60,000—and an ADP figure that surpassed expectations by 62,000. Additionally, the ISM Manufacturing index posted its most impressive result since late 2022, landing at 52.7 compared to the predicted 52.5. These strong fundamental indicators were reinforced by a televised statement from President Trump, who suggested the conflict with Iran could persist for several more weeks, thereby sustaining a consistent appetite for safe-haven investments.

A dramatic shift in momentum occurred between April 6 and 8, precipitated by an unexpected truce between Washington and Tehran. The agreement, which involved Iran reopening the Strait of Hormuz during a fourteen-day pause in fighting, prompted investors to rapidly exit long-dollar trades. This geopolitical breakthrough caused a retreat in energy prices and a decline in Treasury yields, leading the DXY to drop almost 2% toward the 98.50 level. This volatility reflected a sudden transition in market sentiment as participants adjusted their outlook to account for a possible reduction in interest rates by the Federal Reserve.

Between April 8 and 13, the dollar remained range-bound as market participants wavered between tentative hope and growing wariness. This period of stagnation was fueled by Iran’s decision to reinstate the blockade of the Strait following Israeli military actions in Lebanon, alongside the failure of weekend negotiations in Pakistan after Tehran stood firm on its nuclear ambitions. Economic indicators released during this window showed March CPI figures matching predictions at 0.9% monthly and 3.3% annually, though the core inflation reading of 0.2% was slightly lower than the anticipated 0.3%. These results suggested that the spike in energy costs had not yet permeated the broader economy. Meanwhile, the latest FOMC minutes revealed a generally cautious approach from policymakers, despite a small group of officials suggesting the possibility of a rate hike for the first time in the current cycle.

The greenback experienced a temporary decline on April 13 and 14 following comments from Vice President Vance, who described the discussions in Pakistan as constructive. This sparked anticipation for further negotiations, while a Producer Price Index reading of 4.0% annually—which came in below the projected 4.6%—alleviated concerns regarding imminent interest rate increases and placed short-term downward pressure on the currency.

During the latter half of the month, the DXY stabilized and began to trend slightly upward as regional tensions resurfaced. The refusal of Iran to participate in subsequent talks, combined with new reports of ships being seized in the Strait of Hormuz and the continuation of the American naval blockade, revitalized the appeal of the dollar as a defensive asset. Economic reports during this stretch remained robust, with retail sales climbing 1.7% monthly to beat the 0.6% forecast, and unemployment claims staying steady between 207,000 and 219,000. Furthermore, a Reuters survey indicated that a majority of economists anticipated no change from the Federal Reserve until at least September. Although the dollar ended the month shy of its initial peaks, the lack of a geopolitical resolution and a static central bank meant that market direction was dictated more by diplomatic news than by economic statistics.

The volatility of the US dollar throughout April was mirrored exactly across other major currencies. Those currencies typically sensitive to market sentiment suffered most during the early surges in safe-haven buying, losing value as the hostilities involving Iran kept traders on the defensive and maintained strong demand for the American dollar.

The announcement of a truce between April 7 and 8 completely altered the market landscape, sparking a widespread move away from the dollar that triggered significant gains for other currencies. As the premium associated with geopolitical risk vanished, investors rushed back into higher-yielding and commodity-related assets. This shift was most apparent in the AUDUSD pair, which pivoted from its lowest point of the month to its peak in just a few days. A similar pattern emerged in AUDCAD, though the Canadian dollar’s own link to energy prices provided a buffer that moderated the pair’s upward trajectory. Meanwhile, AUDNZD experienced more instability, fluctuating sharply alongside shifting diplomatic news as the two currencies competed for dominance before the Australian dollar eventually finished the month in a stronger position. Even as the temporary peace began to dissolve and the greenback tried to regain momentum during the final two weeks, risk-correlated currencies displayed notable strength. They managed to preserve most of the progress made during the truce, entering a period of consolidation near their monthly peaks instead of giving back their gains. Ultimately, the dollar’s late-month rally lacked the strength necessary to reverse the substantial losses it sustained during that short-lived window of diplomacy.

Gold began the month at a high valuation due to its status as a refuge, but the truce declared on April 7–8 caused an immediate reversal in its fortunes. As the premium linked to geopolitical instability evaporated, the precious metal dropped sharply in value. This downturn was temporary, however, as the failure of negotiations in Pakistan, the continued closure of the Strait of Hormuz, and rising energy costs restored confidence in the metal. By April 17, gold had climbed to a monthly high near $4,880. This momentum soon faded as a strengthening dollar and inflation concerns tied to oil prices reinforced expectations of sustained high interest rates, which diminished the asset’s attractiveness. A significant decline occurred following the Federal Reserve’s April 29 announcement, which saw three officials object to language suggesting future rate cuts. This move pushed Treasury yields and the dollar higher, causing gold to drop toward $4,520. On the final day of April, the metal staged a modest recovery above $4,600 as the dollar pulled back from its recent peaks. Despite this late-month stabilization, gold finished the period significantly lower than its mid-month highs, having spent the month caught between its functions as a shield against conflict and its sensitivity to interest rate policy.

As April concluded, the global financial landscape remained firmly under the influence of the unresolved standoff in the Middle East, leaving market participants in a state of high alert. While economic data continues to show surprising domestic resilience in the United States, the traditional relationship between fundamental statistics and asset pricing has been frequently overshadowed by the immediate impact of diplomatic headlines. This environment has created a complex tug-of-war for the Federal Reserve, which finds itself balancing a robust labor market against the inflationary pressures of a persistent energy shock.

Moving into May, the primary focus remains on the stability of the Strait of Hormuz and the potential for a renewed diplomatic breakthrough, as any shift in the geopolitical status quo will likely be the catalyst for the next major trend in currency and commodity markets. Without a definitive resolution to the conflict or a clear pivot from central bankers, the market enters the new month characterized by cautious consolidation and a continued reliance on safe-haven liquidity.