Overview

During February, the global financial landscape was primarily defined by the intersection of shifting central bank policies, American legislative volatility, and rising international friction. While the confrontation between the U.S. and Iran remained a fluid and unpredictable factor, this analysis prioritizes fundamental economic indicators over the immediate geopolitical developments in the Middle East. Markets experienced significant volatility as the Reserve Bank of Australia implemented its first rate increase in more than twenty-four months, contrasted by an unexpectedly cautious stance from the Reserve Bank of New Zealand. Simultaneously, the Federal Reserve faced the difficult challenge of managing persistent inflationary pressures alongside cooling economic expansion. Investors maintained a high demand for safe-haven assets following the U.S. Supreme Court’s decision to invalidate the IEEPA tariff structure, which prompted the Trump administration to quickly transition toward a comprehensive 15% global import tax. These domestic policy shifts, combined with the lack of progress during nuclear negotiations in Geneva, created a climate of deep uncertainty and conflicting market signals.

The U.S. dollar began the month in a weakened state after a substantial decline in January, yet it staged a robust early comeback fueled by aggressive Federal Reserve commentary, fiscal support measures, and exceptionally strong manufacturing data. Throughout the rest of February, the currency moved through four separate cycles characterized by an opening surge, a deep retracement, a vigorous recovery, and finally a volatile period of consolidation. By the close of the month, the dollar had largely retained the gains from its initial rally, though the underlying macroeconomic environment remained just as fragmented and debated as it was at the start of the period.

Between February 2 and 5, the US Dollar Index strengthened from the high-96 level toward the 98.00 mark, propelled by a trio of converging catalysts. Investors reacted to Kevin Warsh’s nomination as Federal Reserve Chair by bracing for a more restrictive monetary policy, as his advocacy for a reduced balance sheet and disciplined easing was viewed as a structural shift toward hawkishness. This upward momentum was further supported by a Senate deal on a government funding package, which effectively eliminated the threat of a shutdown and improved overall market sentiment.

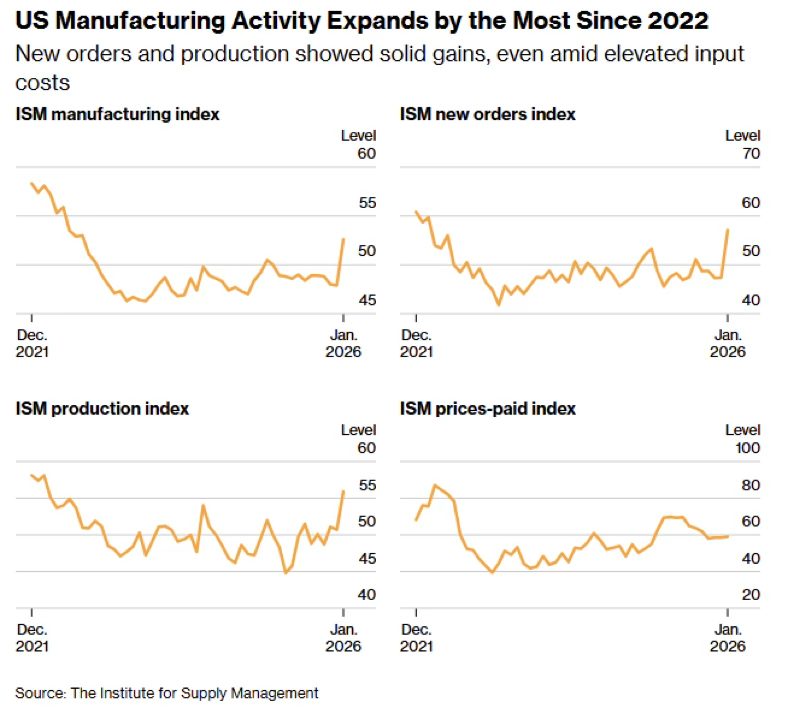

The most significant driver of this rally was the January ISM Manufacturing PMI, which jumped to 52.6 and surpassed the projected 48.5. This figure represented a sharp increase from the previous month and signaled the manufacturing sector’s first return to growth in a year. Accompanying this data, Federal Reserve officials maintained a firm tone by indicating that further interest rate reductions would require more definitive proof of cooling inflation. Meanwhile, the ISM Services PMI remained resilient at 53.8, confirming that the wider economy continued to expand and providing additional justification for the dollar’s appreciation.

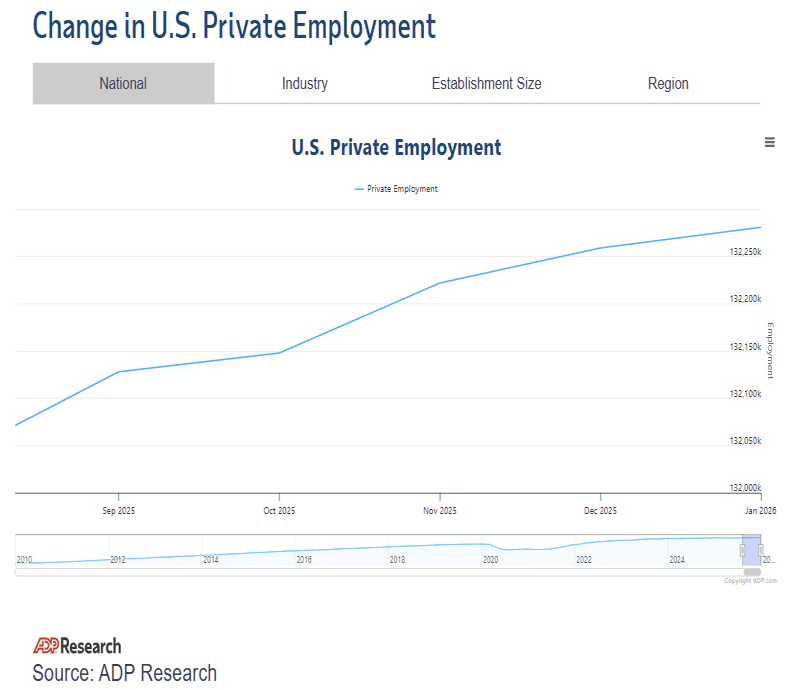

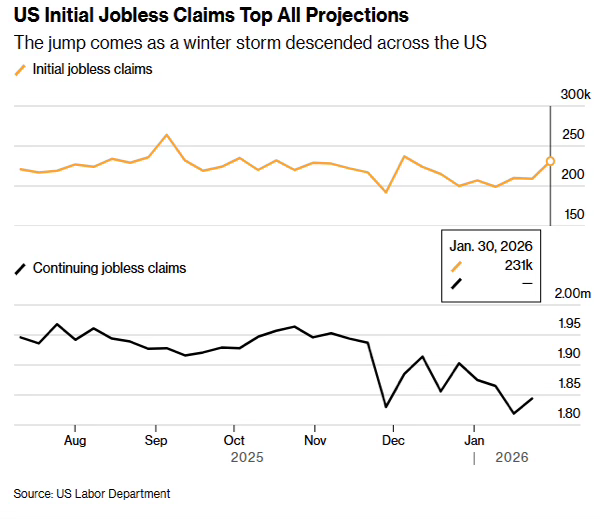

The market sentiment shifted abruptly between 6 and 11 February, pulling the US Dollar Index down to its monthly low near 96.20. This decline was triggered by a series of disappointing economic indicators, starting with January’s private payroll data, which revealed a mere 22,000 new jobs against an expected 48,000. Further pressure came from weekly jobless claims, which climbed to 231,000 and exceeded both the anticipated 212,000 and the previous reading of 209,000. Additionally, December’s retail sales figures remained completely flat, missing the projected 0.4% growth and suggesting that consumer spending had lost significant traction as the year concluded.

These weak domestic data points were exacerbated by reports indicating that Chinese regulators were encouraging local institutions to scale back their holdings of US Treasuries. This development sparked fears regarding a structural decline in international demand for dollar-denominated assets. Consequently, the DXY broke firmly below the 97.00 threshold as investors increased their bets on a more accommodative interest rate environment while awaiting the delayed January employment report.

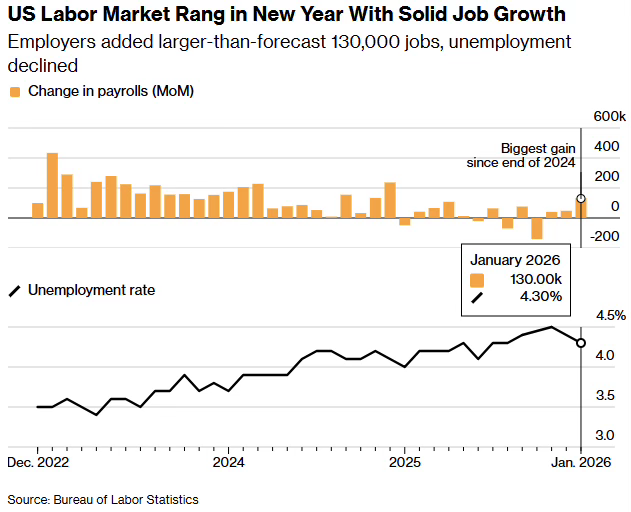

The recovery was both rapid and substantial, as the US Dollar Index reversed its previous losses between 11 and 19 February. During this period, the DXY climbed from below 96.30 to reach the 97.70 level, spurred by a series of critical economic data points. The January nonfarm payroll report was the primary catalyst, revealing 130,000 new jobs—a figure that nearly doubled the anticipated 70,000. This labor market strength was further evidenced by the unemployment rate dropping to 4.3% and average hourly earnings increasing by a slightly elevated 0.4% on a monthly basis. Collectively, these figures represented the most robust employment performance since late 2024 and significantly altered the currency’s trajectory.

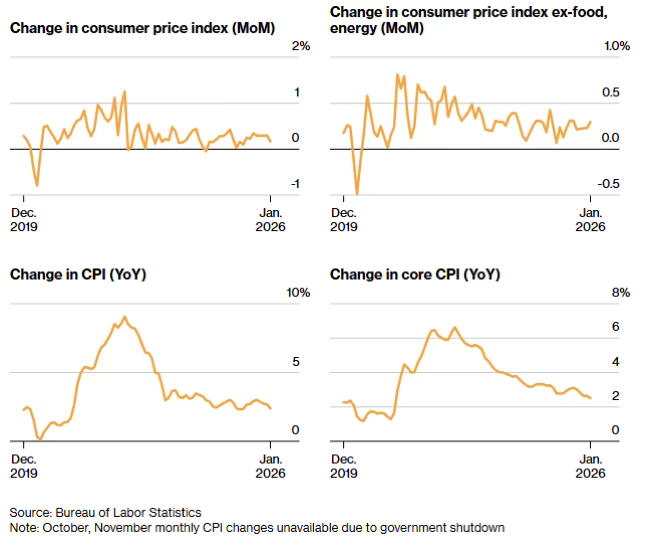

Two days afterward, the January Consumer Price Index provided a perfectly aligned set of data, as headline inflation moderated to 0.2% monthly and 2.4% annually. Both figures came in below expectations, while the core inflation rate remained steady at 2.5% year-on-year, marking its lowest point since April 2021. This specific mix of a durable job market and receding inflationary pressure bolstered the argument for the Federal Reserve to maintain current rates without sparking fears of an economic downturn. Mid-week, the release of the FOMC minutes further supported this less-accommodative outlook, revealing significant internal disagreement among policymakers regarding the timing and requirement of additional rate cuts. Consequently, market expectations for the initial interest rate reduction were pushed back decisively toward June.

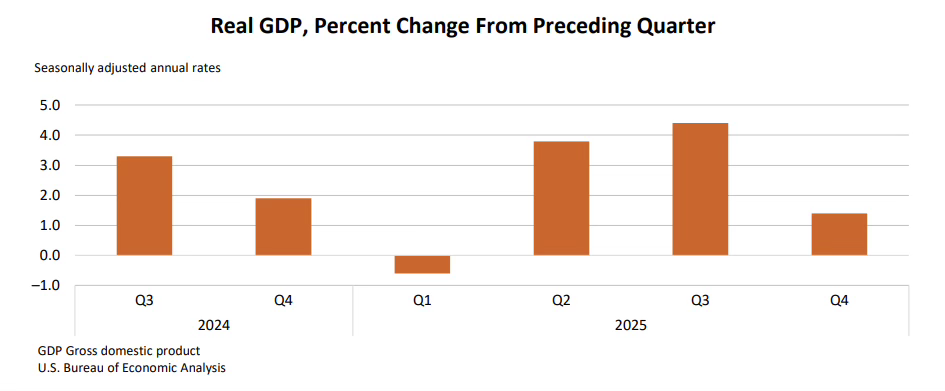

The closing period of February was characterized by significant intraday volatility as the US Dollar Index fluctuated between 97.00 and 97.80 without finding a clear trajectory. A pivotal shift occurred on 20 February when the fourth-quarter GDP was reported at an annualized rate of 1.4%, failing significantly against the projected range of 2.2% to 2.8% and marking a sharp slowdown from the 4.4% growth seen in the third quarter. This economic cooling was complicated by December’s core PCE figures, which climbed to 3.0% annually and 0.4% monthly, exceeding market expectations.

The conflicting nature of these data points—suggesting both slowing growth and stubborn inflation—made it challenging for investors to establish a firm directional bias. This uncertainty was compounded by a 6-3 Supreme Court ruling that invalidated the administration’s tariff authority under the IEEPA. This legal decision effectively eliminated a primary source of structural inflationary pressure, causing the DXY to momentarily break below its session lows as markets reassessed the long-term price outlook.

The greenback’s retreat remained limited as the administration swiftly introduced a 15% global import duty through different legal channels, essentially swapping one type of trade ambiguity for another. As the month drew to a close, Federal Reserve officials consistently advocated for maintaining current interest rates, pointing to inflation levels hovering near 3% and a durable employment sector. Consequently, the US Dollar Index ended February in the upper-97 range, marking a recovery from its January lows. However, this rebound was tempered by lingering concerns over persistent inflation, lackluster economic growth, and an evolving trade policy environment.

In this climate, the most significant market shifts occurred outside of the primary currency pairs. Instead, the Australian dollar crosses and gold emerged as the primary drivers of portfolio performance. These movements were fueled by a combination of a hawkish stance from the Reserve Bank of Australia, an unexpectedly cautious tone from the Reserve Bank of New Zealand, and a heightened global demand for safe-haven assets, which collectively overshadowed many traditional market leaders.

AUD/CAD

The AUDCAD pair exhibited a pronounced upward trend throughout February, appreciating by approximately 2.5% as it benefited from a starkly contrasting monetary policy environment. This movement was underpinned by a strategic shift from the Reserve Bank of Australia, which returned to a cycle of rate hikes, while the Bank of Canada maintained a steady, unchanged stance. This divergence created a persistent structural advantage for the pair, allowing it to sustain gains despite the broader market fluctuations witnessed during the month.

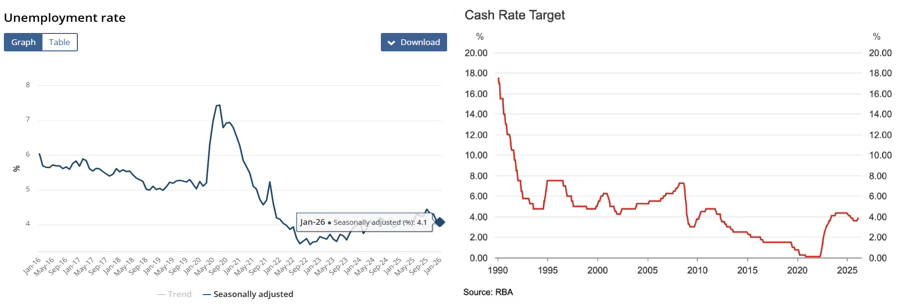

During the initial days of February, AUDCAD experienced a significant climb of approximately 1.75% as investors positioned themselves ahead of a widely anticipated move by the Australian central bank. This momentum culminated on 3 February when the Reserve Bank of Australia implemented a 25-basis-point increase, bringing the cash rate to 3.85%. This marked the first such hike since late 2023 and was driven by evidence that underlying inflation remained both widespread and stubborn. Specifically, the trimmed mean CPI had reached 3.4% annually, exceeding the bank’s established target range, while the labor market showed further tightening with unemployment dropping to 4.1%. Accompanying the rate decision was an upward revision of inflation forecasts, with the RBA now expecting headline CPI to reach a peak of 4.2% by the middle of 2026. This clear shift toward a more restrictive policy stance triggered a sharp appreciation in the Australian dollar.

The initial upward move proved fleeting. From 3–6 February, AUDCAD surrendered the majority of its gains, dropping roughly 1.41% as investors engaged in a typical “sell-the-fact” reaction once the rate hike was confirmed. With the Australian tightening cycle already factored into prices and the US dollar staging a powerful recovery—buoyed by strong manufacturing data and hawkish sentiment surrounding the Fed—the Australian dollar weakened more rapidly than its Canadian counterpart, causing the cross to pull back sharply over just two trading sessions.

Subsequently, the pair embarked on a more persistent climb. Between 6 and 12 February, AUDCAD rose back toward the 0.968 level and stabilized, though this phase was primarily fueled by Canadian dollar depreciation rather than renewed Australian strength. The catalyst was Canada’s January labor report, which revealed a surprising loss of 25,000 jobs, contrasting sharply with the expected 7,000 gain. The manufacturing sector was particularly hard hit, losing 28,000 positions amid ongoing trade and tariff pressures, while Ontario alone saw a significant reduction of 67,000 jobs. Although the headline unemployment rate technically dipped to 6.5%, markets quickly recognized that this was due to 119,000 individuals leaving the workforce rather than an increase in hiring. This disappointing data solidified the view that the Bank of Canada would remain on hold at 2.25% for the foreseeable future, weighing on the CAD and providing a lift to the AUDCAD exchange rate.

During the final stretch of February, the AUDCAD pair entered a consolidation phase, fluctuating within a range of 0.960 to 0.975 as both currencies lacked the momentum to break out. A key update arrived on 17 February with Canada’s January inflation data, which showed headline CPI at 2.3%—slightly below the anticipated 2.4%. More notably, the trimmed mean core inflation measure dropped significantly to 2.4% from 2.7%, reaching its lowest level since April 2021. This softer inflation reading exerted mild downward pressure on the Canadian dollar and provided occasional support to the pair.

Despite this, the exchange rate remained largely range-bound as investors weighed two competing narratives. The Reserve Bank of Australia indicated that while more rate hikes remained a possibility, such moves would be strictly contingent on upcoming data. Meanwhile, the Bank of Canada’s upcoming meeting on 18 March offered few immediate reasons for a shift in CAD sentiment. AUDCAD ended the month positioned near 0.972, maintaining its overall monthly gains as markets continued to price in the starkly different policy paths of the two central banks.

AUD/NZD

Throughout February, AUDNZD experienced a gain of roughly 2.7%, rising from the 1.155 level to finish the month near 1.188. This upward trend was fueled by an increasing policy gap between a more aggressive Reserve Bank of Australia and an unexpectedly cautious Reserve Bank of New Zealand, which provided a consistent tailwind for the pair.

The momentum began early in the month following the RBA’s decision on February 3 to increase the cash rate by 25 basis points to 3.85%, marking its first hike since late 2023. AUDNZD climbed steadily during the first two weeks as markets adjusted to the shifting interest rate differential between the two nations. This policy shift was supported by strong domestic data, including December quarter figures showing headline inflation at 3.6% and the trimmed mean at 3.4%. Both indicators exceeded the central bank’s target range and its previous November projections, confirming that inflationary pressures remained more persistent than anticipated.

With the unemployment rate dropping to 4.1% in December—the lowest level recorded since May—the RBA Board characterized labor market conditions as remaining somewhat constrained. This evidence-based shift toward a more hawkish policy stance provided the necessary momentum for AUDNZD to climb, reaching the 1.180 level by February 12.

A period of brief stabilization followed during the middle of the month, with the exchange rate pulling back toward 1.170 as investors adjusted their holdings in anticipation of the February 18 Reserve Bank of New Zealand policy update. This temporary support for the New Zealand dollar stemmed from fourth-quarter inflation data for 2025, which showed a yearly increase of 3.1%. Since this figure sat slightly above the central bank’s preferred 1–3% target range, it sparked widespread market expectations that a new cycle of interest rate hikes might be imminent.

The Reserve Bank of New Zealand’s actual announcement completely overturned market expectations, sparking a fresh rally in the currency pair as the month drew to a close. In her first Monetary Policy Statement, Governor Anna Breman maintained the Official Cash Rate at 2.25% as predicted, but her rhetoric was significantly more cautious than investors had anticipated. While she noted that headline inflation had slightly exceeded the target range, she voiced certainty that inflationary pressures would naturally recede toward 2% over the next year without requiring immediate policy intervention. To justify this patient approach, she highlighted several cooling factors, including an unemployment rate that remained high at 5.4%, a slowdown in household consumption, and persistent weakness in the housing market.

The most significant impact came from the central bank’s updated interest rate projections, which pushed the first anticipated rate hike back to at least late 2026. The new outlook suggested a very gradual tightening phase, with the rate only expected to reach 3% by 2028—a far more conservative path than the two immediate hikes investors had previously anticipated. In response, the New Zealand dollar fell by more than 1.3% against the US dollar during the session, while AUDNZD surged back above the 1.185 level, eventually ending February near 1.187. Ultimately, the month’s primary market driver was the stark contrast in policy: an Australian central bank actively raising rates versus a New Zealand counterpart showing no immediate intention to follow suit.

AUD/USD

AUDUSD experienced an appreciation of approximately 2.4% during February, driven by the tension between a hawkish shift from the Reserve Bank of Australia and a fluctuating American economic landscape. The pair saw significant volatility as the Australian dollar benefited from a newly aggressive policy stance, while U.S. indicators alternated between signs of strength and unexpected softness, ultimately resulting in a clear net gain for the Aussie.

The month’s commencement perfectly illustrated the competing forces at play. On February 3, the Reserve Bank of Australia’s decision to raise interest rates to 3.85%—a move backed by a 4.1% unemployment rate and 3.4% annual trimmed mean inflation—triggered a sharp rally in the pair. However, these gains were nearly erased within 48 hours as the US dollar regained momentum. This American recovery was fueled by the ISM Manufacturing index jumping to 52.6, marking its first move into expansionary territory in a year, and a legislative agreement in the Senate that averted a government shutdown. Consequently, by February 5, AUDUSD had retreated from its highs to trade virtually flat compared to its opening price for the month.

The subsequent period saw a rapid and consistent retreat for the US dollar, propelling AUDUSD to its highest levels of the month. Between February 6 and 12, a string of weak American economic reports—highlighted by ADP payrolls adding only 22,000 jobs against a 48,000 forecast, stagnant retail sales, and jobless claims rising to 231,000—undermined the brief dollar rally. These disappointments shifted the market narrative, allowing the pair to surge toward 0.715 by February 12, as the Australian dollar’s own hawkish momentum further accelerated the climb.

Following that phase, the pair entered a broad and volatile range that lasted through the end of the month. On February 11, the delayed January nonfarm payrolls report showed 130,000 new jobs—nearly doubling expectations—while the subsequent consumer price index reading revealed headline inflation at 2.4%. This combination of labor market durability and easing price pressures provided the US dollar with enough support to limit further gains for the Australian dollar. However, the greenback faced renewed pressure after fourth-quarter GDP missed forecasts, growing at just 1.4% compared to the anticipated 2.2–2.8%. This weakness was later offset on February 20 by a core PCE reading of 3.0%, which reignited concerns about stagnant growth paired with high inflation and solidified expectations that the Federal Reserve would keep interest rates unchanged. AUDUSD fluctuated between 0.705 and 0.715 for the remainder of the month, ultimately closing near 0.712. This overall increase was less the result of a single market driver and more a reflection of a hawkish Australian central bank contrasting with a US economy hampered by conflicting data.

Gold

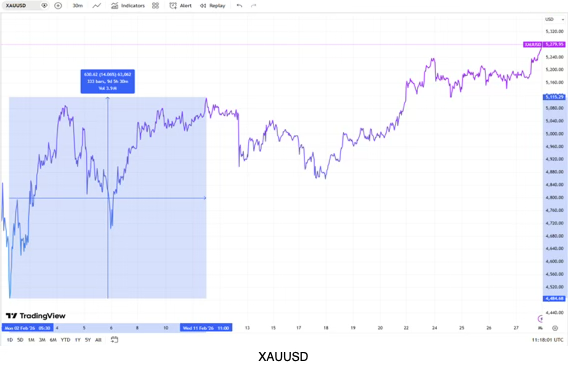

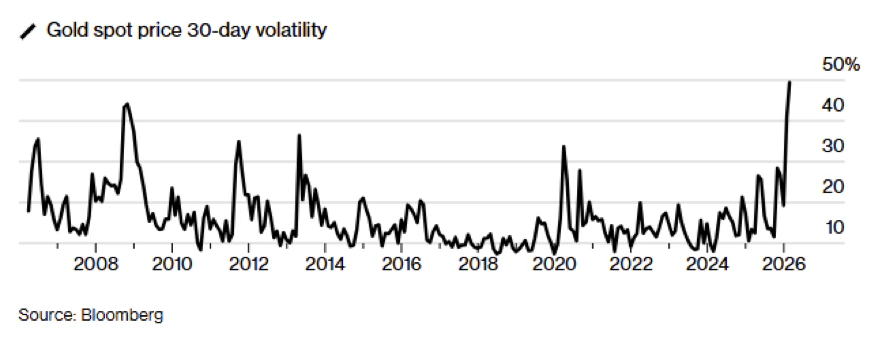

The month of February began in the aftermath of a volatile period for gold, which had just endured two sessions of extreme selling. After reaching a historic peak near $5,595 on 29 January, the metal suffered a collapse of approximately 9% the following day. This sharp reversal was triggered by the nomination of Kevin Warsh as the next Federal Reserve Chair, a move that investors interpreted as a commitment to maintaining central bank independence and rolling back the “debasement” premium that had previously supported the gold rally. The resulting surge in the U.S. dollar led to widespread margin calls, forcing a rapid liquidation of positions and leaving the gold market in a vulnerable state at the start of the new month.

The downward pressure persisted into 2 February, pushing the total peak-to-trough decline to approximately 21% in just two sessions. This historic rout left gold prices languishing near $4,400–$4,480, effectively erasing trillions in market value as leverage was flushed out of the system.

Adding to the metal’s woes, the ISM Manufacturing report released that same day delivered a headline print of 52.6—the first expansionary reading (above 50) for the sector in a year. This stronger-than-expected economic data provided a fresh catalyst for the US dollar’s recovery, further stifling any attempts at a “dead cat bounce” and reinforcing the narrative that the new Fed leadership would have the economic breathing room to maintain a more restrictive policy.

ollowing that established floor, the metal staged a powerful recovery through the second week of February. This second leg of the rally was fueled by a “perfect storm” of macro and geopolitical catalysts that saw gold reclaim the $5,100 handle by 11 February.

The advance was driven by two primary factors:

- Deteriorating US Macro Data: A sequence of soft reports—most notably an ADP private payrolls print of just 22k (well below the 48k forecast) and stagnant retail sales—undermined the “higher-for-longer” dollar narrative. This prompted a swift unwinding of the post-Warsh nomination dollar surge.

- Escalating Middle East Tensions: Safe-haven demand intensified as the US-Iran relationship reached a breaking point. Washington initiated its largest military mobilization in the region since 2003, deploying massive air and naval assets to the Middle East as a “pressure tactic” ahead of the high-stakes nuclear negotiations in Geneva.

By mid-month, the combination of a weakening dollar and the shadow of potential conflict had restored gold’s status as the preferred hedge, allowing it to recover more than half of its late-January losses.

The gold market’s recovery hit a plateau mid-month, with the metal oscillating within a roughly 5% band through 20 February. This period of indecision was driven by hawkish signals from the Federal Reserve, specifically via FOMC minutes and Governor Waller’s suggestion that the central bank might hold rates steady in March, which effectively capped the metal’s upward momentum. The month’s most decisive turning point arrived on 20 February, when the Supreme Court invalidated the administration’s IEEPA-based tariff authority. While initially viewed as a relief trade for broader markets, the same day’s economic data—a dismal Q4 GDP print of 1.4% alongside a “hot” core PCE reading of 3.0%—presented a stagflationary dilemma that moved gold back into the spotlight. This bullish setup was further cemented by the President’s immediate pivot to a 15% global import surcharge, which restored the policy uncertainty premium that had characterized the start of the year.

As February drew to a close, gold climbed an additional 5% to finish near $5,280, representing an 11.70% gain from its early-month lows and marking its fourth consecutive weekly advance. This final push was fueled by heightened geopolitical anxiety following the 26 February State of the Union address, in which the President explicitly mentioned potential military action against Iran as nuclear talks in Geneva remained inconclusive. Institutional support reinforced the rally, with JP Morgan raising its long-term targets on 25 February and maintaining a $6,300 year-end forecast for 2026. The bank noted that while retail sentiment fluctuated, the underlying bull case remained firm due to structural central bank buying and significant ETF inflows, which had already reached approximately 59 tons for the year.

An important operational detail emerged during this period, as a noticeable divergence developed between the portfolio’s total balance and its equity curves. This gap was the result of elevated floating drawdown, primarily a byproduct of the intense and sustained trending behavior seen in both the AUDCAD and AUDNZD pairs. Instead of liquidating core positions into these extended market moves—which could have compromised the long-term integrity of the strategy—the decision was made to hedge roughly 85% of the total exposure. This approach successfully insulated the portfolio from significant directional risk while keeping the underlying strategy structure intact. These hedge positions were not static; they were actively traded and monetized during short-term market retracements, providing a source of realized gains that bolstered overall performance throughout the month.

The temporary gap between equity and balance is a direct result of unrealized losses on open core positions, representing a calculated risk management strategy in a trending market rather than a change in underlying conviction. This approach allowed the portfolio to navigate the aggressive Australian dollar moves of February without forcing a premature exit from the broader strategy. Looking forward, although the Australian dollar crosses remained strongly supported through the end of the month, the price action has become increasingly extended compared to historical norms. While there is still potential for further gains, the likelihood of a medium-term peak is rising. Consequently, high levels of hedge coverage are being maintained as the market is monitored for signs of trend exhaustion. As seen in the last few days, with both NZDCAD and AUDCAD beginning to taper and partially reverse their recent advances, automated systems have already started to scale back these hedges to align with the shifting momentum.