Overview

The recent 43-day US government shutdown, spanning from October 1 to November 12, established a new, unprecedented duration. This protracted closure disrupted the typical schedule of macroeconomic data releases, compelling investors to navigate a climate of heightened uncertainty by relying on fragmented private-sector indicators and conflicting statements from the Federal Reserve.

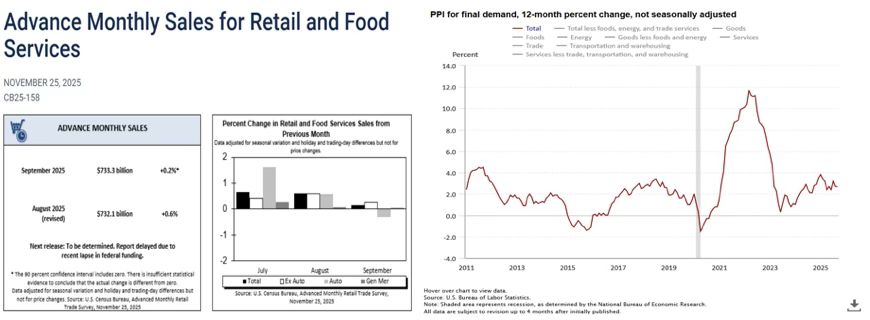

The Bureau of Labor Statistics (BLS) formally canceled the October Consumer Price Index (CPI) and Employment Situation reports due to insufficient data collection. Other key releases, including real earnings and Gross Domestic Product (GDP) estimates, were deferred until December. Only a few postponed publications, such as the delayed September jobs report released on November 20, were successfully rescheduled.

With severely limited visibility into US inflation, labor market conditions, and economic growth, markets became significantly more responsive to changes in Fed guidance and broader macro headlines. Key November releases are now anticipated for mid-to-late December, likely accompanied by data-quality disclaimers—especially for the CPI. This sets the stage for a concentrated wave of data dissemination in the near term.

Amidst this backdrop of limited macroeconomic visibility and unusually high policy uncertainty, the US dollar (DXY) exhibited significant intra-month volatility in November, ultimately closing the period near its starting point. This performance reflected a dynamic tension between fluctuating Federal Reserve expectations, persistent political uncertainty, and the gradual return of US macroeconomic data following the government shutdown.

The month began with the dollar on a strong trajectory. Following a hawkish interest rate adjustment by the Fed in late October and concurrent easing of US-China trade tensions, the DXY approached the 100 level. Early-month pricing indicated that markets were significantly discounting the probability of a December rate cut. On November 3–4, the index briefly surpassed 100 for the first time since August, supported by risk-aversion sentiment and a repricing of Fed expectations driven by mixed but generally cautious messages from policymakers. At this point, the probability of a December rate cut, which had been above 90%, was trimmed to the mid-60% range, providing a temporary boost to the dollar.

However, this momentum dissipated as the month unfolded. The prolonged government shutdown, now the longest in US history, introduced considerable uncertainty, exerting downward pressure on the dollar despite typically supportive risk-off conditions. The absence of key data, coupled with soft consumer sentiment and concerns regarding equity market valuations, amplified investor anxiety. Consequently, the dollar experienced a sharp decline before stabilizing into a narrow consolidation range by November 7, where it remained range-bound until mid-month.

The continued stream of softening data releases solidified market expectations for a December rate cut. On November 28, the Personal Consumption Expenditures (PCE) deflator—the Federal Reserve’s preferred inflation gauge—was released, showing the core reading rising only 0.1% month-over-month (MoM) in September, with the year-over-year (YoY) measure holding steady at 2.6%. This data confirmed easing inflationary pressures, leading futures markets to fully price in a 100% probability of a December rate reduction.

The dollar reacted by falling sharply to its lowest point since October 22. In the final days of the month, the DXY drifted within a narrow range between 99.10 and 99.40. Overall, the dollar was essentially flat for the month, as the initial forces of uncertainty and risk-off sentiment during the shutdown offset the impact of the late-month data-driven sell-off. The dollar ultimately closed the month at 99.40, marking a marginal 0.2% decline.

The November trading session was defined by a significant shift in market drivers. The initial period was dominated by the unprecedented political uncertainty of the prolonged government shutdown and the resultant data vacuum. The latter part of the month, however, saw the market move to price in a full probability of a rate cut in response to the belated release of soft US economic data. This dynamic ultimately placed the dollar under persistent pressure throughout the period.

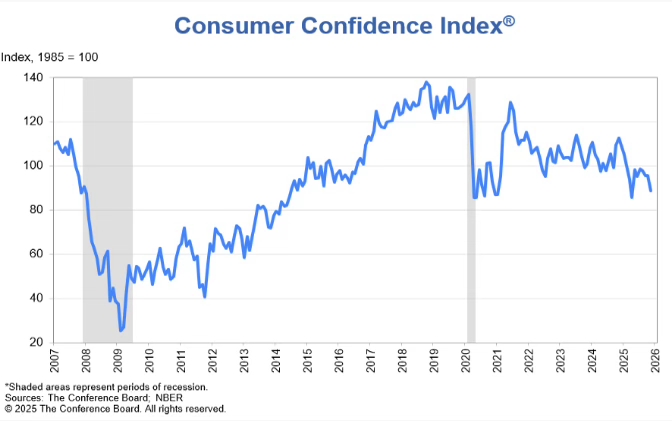

Consumer confidence also continued its decline. Moreover, ADP data revealed that private employers shed an average of 13,500 jobs over the four weeks ending November 8, representing a marked deterioration from the prior negative 2,500 pace. Collectively, these indicators reinforced the narrative of slowing demand and a weakening labor market, which further weighed on the dollar toward the close of the month.

Further pressure was exerted on the dollar by dovish Federal Reserve rhetoric, rising speculation that Kevin Hassett—a lower-rate-leaning candidate favored by the Trump administration to potentially replace Jerome Powell—could become the next Fed Chair, and a temporary de-escalation of Ukraine-related geopolitical tensions. By November 28–29, the DXY had declined into the 99.0–99.1 range, positioning for its weakest weekly performance since July, although it remained broadly unchanged over the full month.

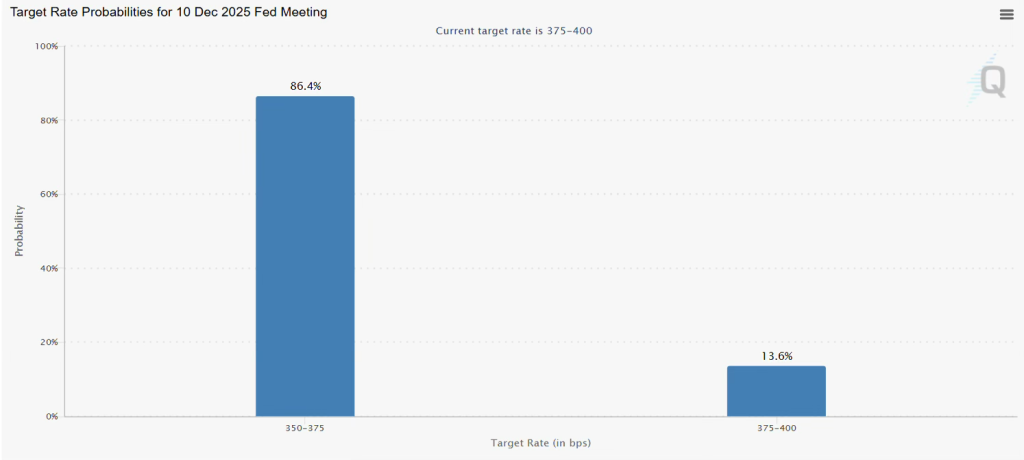

In the final days of November, the CME FedWatch Tool assigned an 87% probability to a 25 basis point rate cut in December, a significant increase from just 49% a few days earlier.

Naturally, this volatile dollar environment influenced the month’s major currency movements.

EURUSD spent November engaged in a broad two-way pattern, ultimately closing the month marginally higher. The repeated shifts in the balance of power between the euro and the dollar were driven by fluctuating Federal Reserve expectations, the ongoing US government shutdown saga, and a cautious yet consistent profile maintained by the European Central Bank (ECB).

The month commenced with the euro under pressure. From November 1–4, EURUSD extended a five-session losing streak as the Federal Reserve’s hawkish October rate adjustment and the sharp reduction in December cut probabilities fueled broad dollar strength. On the euro side, the ECB’s October decision to keep rates on hold for a third consecutive meeting, coupled with its communication that inflation was near target, growth remained positive, and policy was “in a good place,” provided some insulation but was insufficient to fully counteract the dollar’s early-month momentum.

The dynamic shifted beginning November 5. As the US government shutdown entered its sixth week and posed the threat of becoming the longest on record, the dollar’s appeal began to wane. EURUSD reversed its preceding decline, driven by improving risk sentiment, expectations for a cautious and data-dependent European Central Bank (ECB), and a rebound in equity markets.

German industrial production delivered a weaker-than-expected result (1.3% MoM versus 3% anticipated), yet the euro maintained its stability. This resilience was supported by the perception that the European Central Bank (ECB) had concluded its rate-hiking cycle for the foreseeable future. Against the backdrop of Wall Street volatility driven by AI-bubble concerns, the absence of crucial US data, sharply weaker US consumer sentiment, and softening near-term US inflation expectations, investors favored the euro over the dollar, even amid a broader risk-off market tone.

By November 13, EURUSD had climbed to a two-week high, settling just above 1.1650. Even though the Eurozone’s industrial production for September fell short of expectations, the conclusion of the 43-day US government shutdown fueled global risk appetite, which maintained downward pressure on the dollar.

A brief pullback in EURUSD occurred between November 17 and 20, driving the pair back below 1.1600. This decline was attributed to a strengthening dollar ahead of the delayed September Non-Farm Payrolls (NFP) release and a reduction in Federal Reserve rate cut expectations, which fell toward approximately 49%. Renewed risk aversion further supported the dollar’s bid, causing the pair to drift lower before entering a consolidation phase.

The final stretch of November decisively favored the euro. Softer US producer prices, weaker US retail sales, and clear evidence of cooling US labor demand pushed the market back toward a firmly dovish outlook for the December Federal Reserve meeting. This data, combined with dovish messaging from senior Fed officials late in the month, revived expectations of an imminent rate cut and weakened the dollar. With US macroeconomic momentum appearing increasingly fragile, the euro concluded the month on a firmer footing.

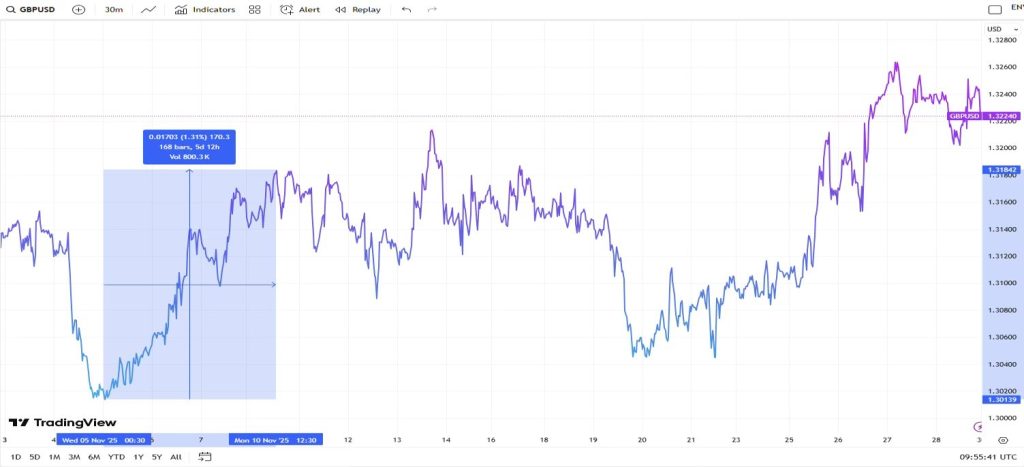

GBPUSD also began November on the defensive as UK fiscal anxieties coincided with a firmer dollar. Chancellor Rachel Reeves’ signals of impending tax hikes and “hard choices” ahead of the Autumn Budget intensified concerns regarding fiscal drag, potentially opening the door for further Bank of England (BoE) easing. Since markets were simultaneously reducing December Fed-cut probabilities, the Pound underperformed during the initial days of the month.

Conditions shifted after November 5. The BoE delivered a dovish hold, revealing a larger-than-expected voting bloc in favor of a rate cut and explicitly citing softer inflation risks and weakening demand. This initially pressured the Pound, but the persistent US government shutdown sufficiently undermined the dollar, allowing GBP to rebound. The recovery, however, was limited by weak UK labor market data—specifically, rising unemployment, falling employment, and easing wage growth—which pushed BoE cut expectations close to the 80% mark.

Sterling experienced a brief spike on November 13 as markets reacted to the prior day’s conclusion of the 43-day US shutdown, which boosted risk appetite and weakened the dollar. However, this move quickly faded. Weak UK Gross Domestic Product (GDP) data, combined with the government’s decision to abandon planned income-tax increases, resurrected concerns regarding fiscal discipline. Concurrently, Federal Reserve officials warned against premature easing, reducing some of the market’s earlier dovish Fed expectations and gently nudging GBPUSD lower once again.

The pair drifted sideways until November 18 before falling sharply on November 19, a move triggered by the release of the UK Consumer Price Index (CPI) for October. The CPI came in exactly as anticipated at 3.6% year-on-year, easing from 3.8% in September. This confirmation of cooling—yet still elevated—inflation reinforced expectations for a December Bank of England (BoE) rate cut. Simultaneously, the dollar gained temporary support as markets prepared for the release of delayed US data following the government shutdown.

However, as the month progressed toward its close, US data releases became increasingly mixed: a strong headline payrolls figure accompanied by a higher unemployment rate was followed by softer Producer Price Index (PPI), weaker retail sales, and clear signs of cooling labor demand. Markets consistently interpreted this combination through a dovish Federal Reserve perspective, which drove up December rate cut probabilities and ultimately weighed on the dollar, thereby supporting the GBPUSD pair.

Sterling gained additional support ahead of the Autumn Budget as expectations mounted that Chancellor Rachel Reeves would take meaningful steps to stabilize the fiscal outlook. The Budget was largely well received, despite downgraded growth forecasts, while Fed-cut probabilities climbed into the mid-80% range. The dollar remained pressured, and GBPUSD continued to firm, eventually stabilizing into a late-month consolidation phase with a stronger underlying tone.

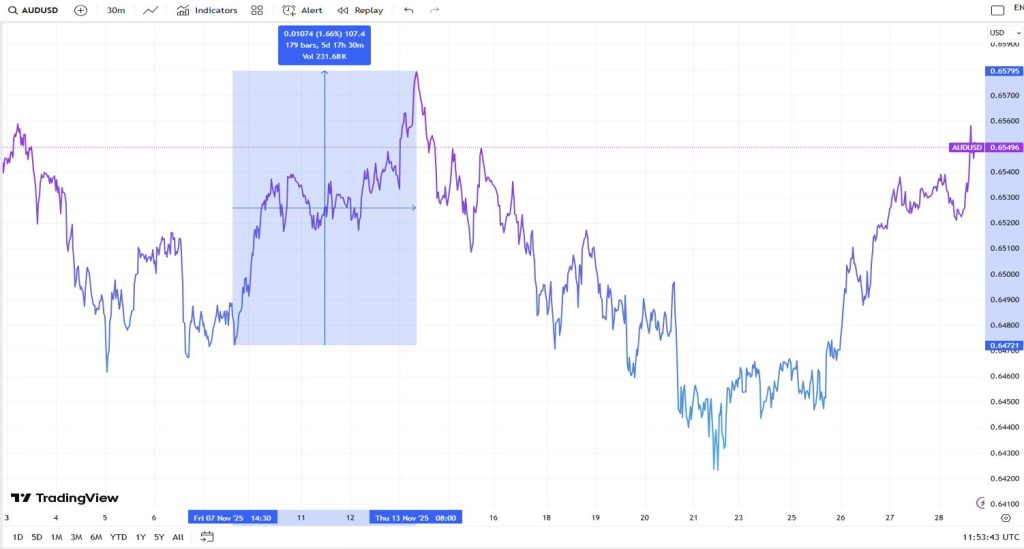

AUDUSD began November under pressure as risk-off sentiment and a firmer US dollar offset the Reserve Bank of Australia’s (RBA) hawkish hold at 3.6%. Although the RBA highlighted persistent inflation and firm wage dynamics, the Australian dollar still declined as markets reduced Fed-cut expectations and global sentiment turned defensive.

Between November 7 and 13, AUDUSD staged a steady rally. Hawkish remarks from RBA officials and a re-acceleration in third-quarter Australian inflation supported the currency. Furthermore, improving Chinese Consumer Price Index (CPI) and PPI readings, alongside Beijing’s temporary easing of export restrictions, provided an additional lift.

The rally extended further on November 13 following the release of strong Australian jobs data, which showed employers adding 42.2K positions and the unemployment rate easing to 4.3%. This reinforced expectations that the Reserve Bank of Australia (RBA) would maintain its current policy stance rather than pivot toward rate cuts. Simultaneously, increasing conviction regarding another Federal Reserve rate cut later in the year exerted downward pressure on the dollar.

The momentum, however, faded after November 13. Between November 13 and 21, AUDUSD drifted lower as the US dollar regained traction. This was driven by Federal Reserve officials pushing back against premature easing, which prompted markets to scale back expectations of a December rate cut. Simultaneously, strong US manufacturing data and soft global risk sentiment—including an equities sell-off driven by AI-valuation concerns—pressured cyclical currencies like the Australian dollar. Broader geopolitical tensions, including renewed strains between China and Japan, added further downward pressure, pushing AUDUSD to new multi-month lows around November 24 despite improving Australian Purchasing Managers’ Index (PMI) readings.

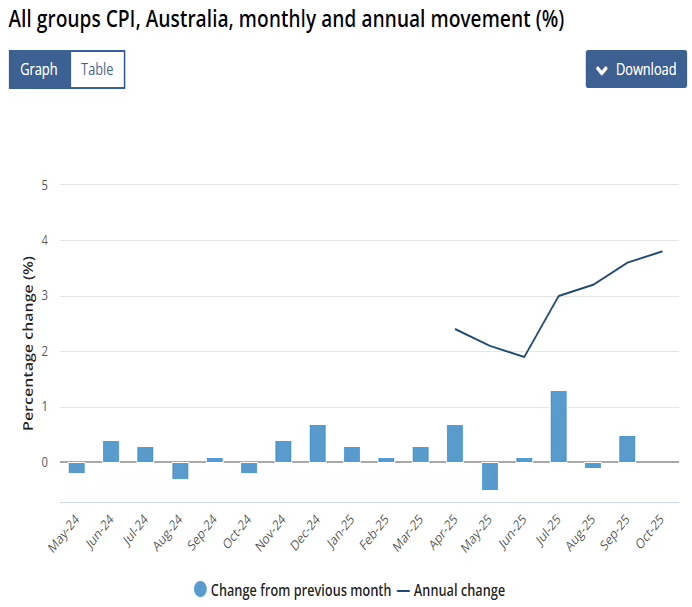

The sentiment decisively shifted again after November 25. AUDUSD rebounded sharply as Australia’s new monthly Consumer Price Index (CPI) measure surprised to the upside at 3.8% year-over-year in October, exceeding market expectations of 3.6% and the previous 3.5%, thereby reinforcing the Reserve Bank of Australia’s cautious stance. Concurrently, US data turned softer. Weaker Producer Price Index (PPI) components, cooling retail sales, deteriorating consumer confidence, and increasingly dovish remarks from several Fed officials drove December cut expectations above 84%, weakening the dollar.

Strong Australian private capital expenditure, which increased by 6.4% quarter-over-quarter (QoQ) and significantly exceeded expectations, provided further support for the Australian dollar (AUD).

By late November, the combination of persistent Australian inflation, firm domestic economic data, and a Federal Reserve increasingly perceived as nearing a dovish policy pivot allowed AUDUSD to trend higher.

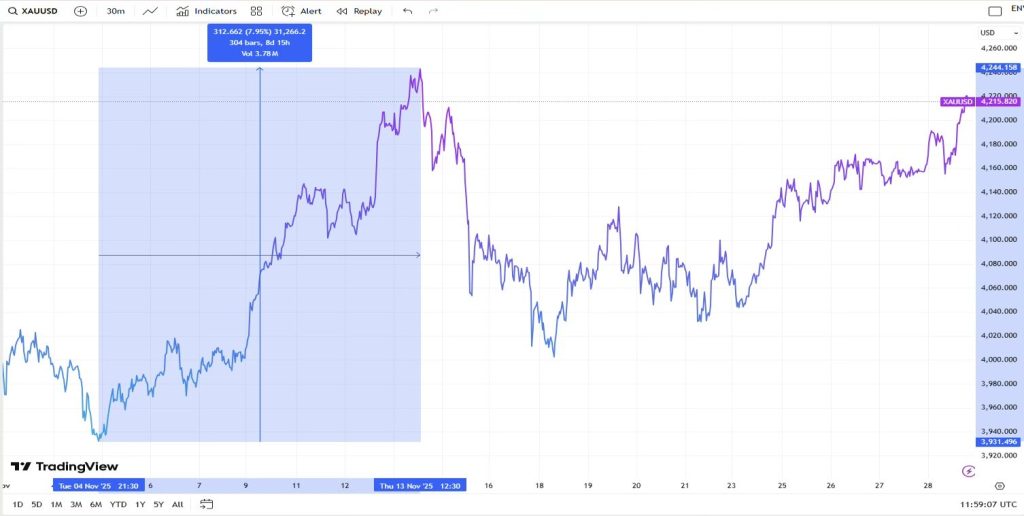

Gold opened November under pressure as a firm US dollar and a cautious Federal Reserve tone kept the metal below the $4,000 threshold. Early weakness was amplified by China’s new Value-Added Tax (VAT) rules, which prompted major state banks to suspend physical gold redemptions and the opening of new retail accounts, temporarily curbing demand from one of the world’s largest bullion markets.

From November 4 to 13, gold climbed steadily. A softer dollar, concerns over the economic fallout from the prolonged US shutdown, and persistent geopolitical tensions all bolstered safe-haven interest. Rising Federal Reserve rate-cut expectations—supported by weak US private-sector jobs data, deteriorating consumer sentiment, and signs of slowing economic momentum—reduced the opportunity cost of holding bullion. By mid-month, gold had rebounded toward three-week highs.

However, Gold reversed course between November 13 and 18 as the US government reopened, safe-haven demand faded, and traders reduced their bets on a December Federal Reserve rate cut. The US–China trade truce further lessened defensive flows, while a firmer dollar and pushback from Fed officials kept the metal under pressure.

Between November 18 and 24, Gold traded within a tight range as markets processed delayed jobs data, a global equities rebound driven by Nvidia’s strong earnings report, and a stronger dollar as investors reassessed the likelihood of near-term easing.

Momentum shifted again after November 24. Stalling US inflation, weaker consumer spending, and a sharp drop in Conference Board confidence revived expectations for a December Fed cut, pushing cut probabilities above 80% and sending gold higher. Additional support was derived from soft Producer Price Index (PPI) components and dovish commentary from multiple Federal Reserve officials, who signaled a readiness to ease policy if labor-market and inflation trends continued to weaken.

By the end of the month, gold was trading firmly above $4,200, supported by an aggressive dovish repricing that took December cut odds close to 87%. While tentative progress on a Russia–Ukraine peace framework modestly capped safe-haven demand, the broader macroeconomic backdrop—cooling US inflation, weakening demand indicators, and rising expectations of Fed easing—kept bullion’s late-month bias decisively upward.

System Breakdown

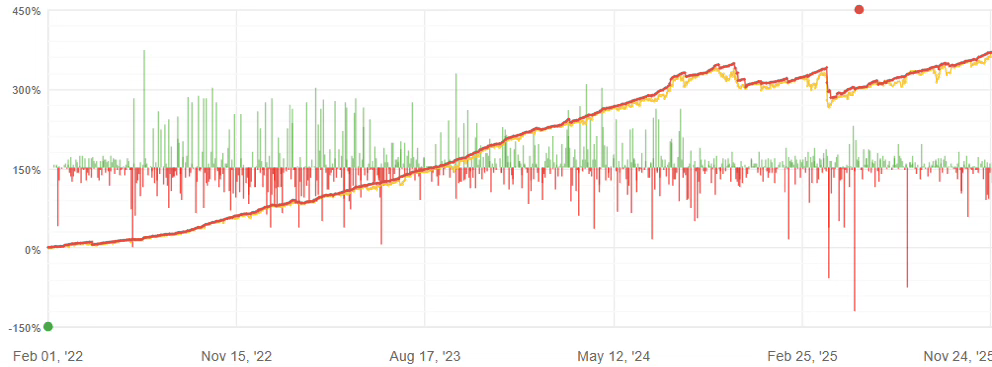

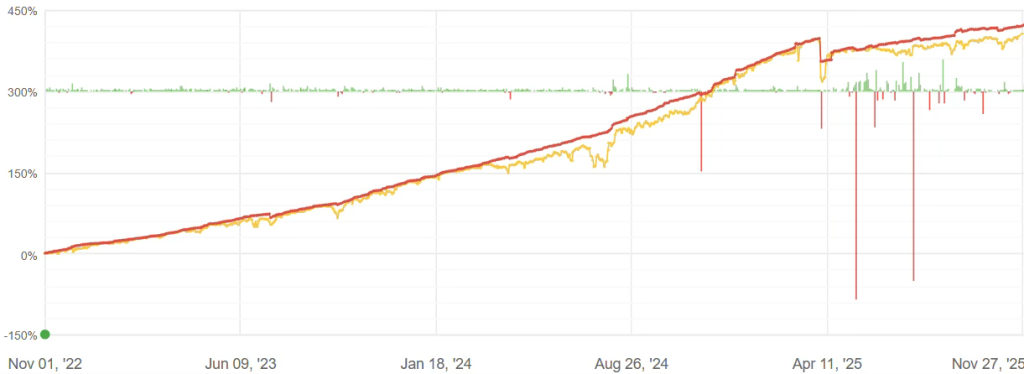

Amid a month defined by missing US macroeconomic data, shifting Federal Reserve expectations, and choppy but ultimately range-bound market conditions, both R-50 and R-10 delivered strong performances in November, returning 3.43% and 3.21%, respectively.

Both systems trade the same subsystems, with the R-10 applying a slight filter on smaller trades to accommodate a lower minimum deposit.

R-50

For R-50, the long/short positions in EURUSD, AUDCAD, and NZDCAD were the primary contributors to profit, while the largest losses were incurred by short positions in AUDNZD, GBPJPY, and NZDUSD.

November’s volatility in USD sentiment—driven by the US shutdown resolution, shifting interest rate expectations, and a late-month dovish repricing—generated clean intraday and multi-day swings that R-50 effectively capitalized on across both long and short legs of EURUSD. Similarly, AUDCAD and NZDCAD provided attractive volatility and mean-reversion setups as markets reacted to China-related news, mixed Australian data, and broad USD softness toward the end of the month.

R-10

Meanwhile, R-10‘s top profit/loss contributors also included EURUSD, USDJPY, and AUDCAD.

During the period, R-50 executed 1,556 trades, achieving a win percentage of 70% with an average holding period of 1 day. In comparison, R-10 executed 358 trades, registering a win percentage of 74% with an average holding period of 3 days.

All subsystems were thoroughly reviewed and re-calibrated at the end of November to ensure consistency and optimal performance, particularly given the prevailing market conditions.

R-X25

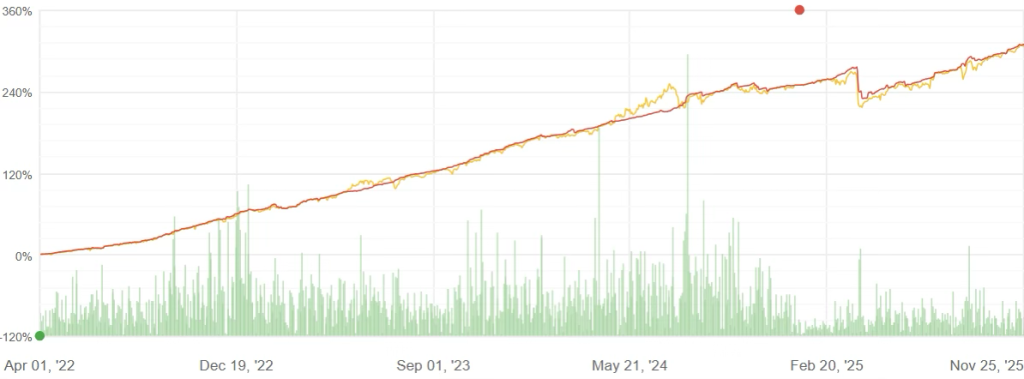

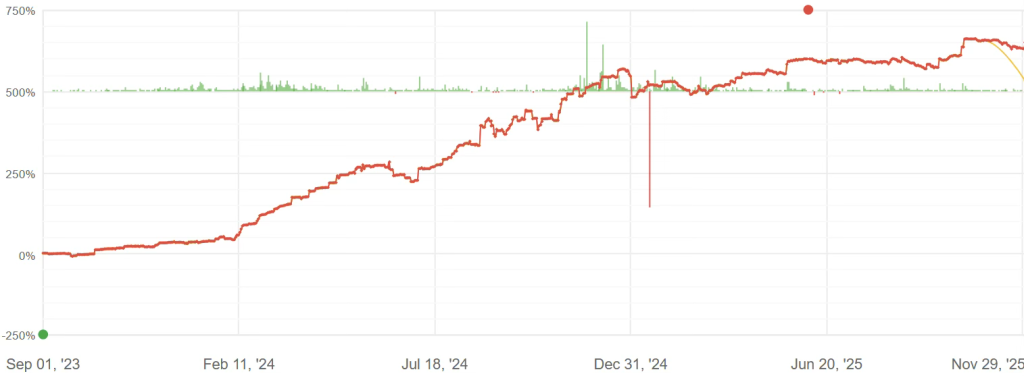

Navigating a month characterized by limited US data visibility, elevated macroeconomic uncertainty, and choppy price action, R-X25 delivered a strong 2.26% return in November.

The system executed 703 trades, achieving a notably high win rate of 72% and an average holding period of 1 day. The Profit Factor—the ratio of total profits to total losses—stood at 2.15, reflecting exceptional system-level efficiency against a complex and data-distorted market backdrop.

The long/short positions in XAUUSD, long positions in EURCHF, and long/short positions in USDCHF were the largest contributors to November’s profit and loss (P&L), with no meaningful detracting trades.

Gold’s pronounced intra-month swings—driven by shifting Federal Reserve cut expectations, fluctuating risk sentiment, and volatile dollar dynamics—allowed the strategy to generate gains on both sides of the trade. Similarly, exposures to CHF-crosses benefited from the franc’s sensitivity to shifting global risk appetite and evolving US rate expectations, providing steady opportunities across both EURCHF and USDCHF.

By November-end, the system maintained substantial exposure in XAUUSD long, XAUUSD short, and NZDCAD long.

R-X5

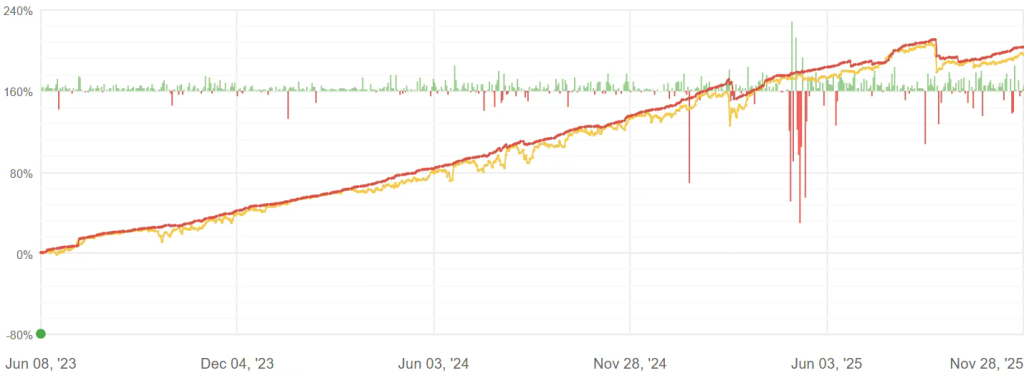

Amid a month marked by limited US data visibility, elevated uncertainty, and uneven price action, R-X5 delivered a solid 1.93% return in November.

The system executed 328 trades, achieving a strong win rate of 75% and an average holding period of 3 days. The Profit Factor—the ratio of total profits to total losses—stood at 1.96, reflecting robust system-level efficiency despite the challenging macroeconomic backdrop.

The long/short positions in EURUSD, GBPUSD, and NZDCAD were the top contributors to November’s profit and loss (P&L), with the AUDUSD long position being the only notable detractor.

The strategy successfully captured both sides of EURUSD and GBPUSD as the market processed shifting Federal Reserve cut expectations, the resumption of US data releases following the shutdown, and a steady but data-dependent stance from the ECB and the Bank of England. EURUSD oscillated as softer US activity data contrasted with a cautious Eurozone outlook, while GBPUSD responded to a mix of UK fiscal updates, cooling domestic momentum, and broader dollar swings. These alternating drivers created a fluid two-way environment that R-X5 systematically navigated across both legs of the trades.

The long/short positions in NZDCAD also contributed meaningfully, as recurring volatility in the New Zealand and Canadian dollars created opportunities throughout the month, driven by uneven domestic data and fluctuations in global risk sentiment.

By November-end, the system’s largest exposures were AUDNZD short, NZDCAD short, and NZDCAD long.

R-C30

R-C30, which maintains balanced long-and-short exposure across BTCUSD and ETHUSD, faced one of the most punishing crypto market environments in recent months, finishing November down only 2.54% despite severe, sustained declines in both major tokens.

The system executed 157 trades, achieving a win percentage of 52% and an average holding period of roughly 8 hours.

There were no positive contributors in November, as both BTCUSD and ETHUSD long/short positions came under pressure. This outcome reflects the extraordinary nature of the month: BTCUSD fell 21.73%, while ETHUSD dropped an even steeper 26.74%, marking one of the sharpest synchronized declines in the two largest crypto assets in recent months. With both markets trending persistently lower and exhibiting very limited meaningful retracements, long-side structures struggled, while short-side gains were repeatedly interrupted by abrupt but shallow relief rallies—a combination that historically occurs only in high-stress, capitulation-type environments. Against this backdrop, R-C30’s modest drawdown of 2.54% is a testament to the system’s resilience.

The system’s exposure by November-end was concentrated in BTCUSD, accounting for almost 61% of the total exposure.

All subsystems were thoroughly reviewed and re-calibrated at the end of November to ensure consistency and optimal performance, particularly in light of the prevailing market conditions.